India Electric Commercial Vehicles (eCVs) Market and Forecast Report (2021–2030) – by Vehicle Type (2-Wheelers, 3-Wheelers, 4-Wheelers, Buses, Trucks), End Use (Logistics, Last-Mile Delivery), and Region Analysis

India Electric Commercial Vehicles (eCVs) Market Size

India’s Electric Commercial Vehicles (eCVs) market has witnessed remarkable expansion between FY2021 and FY2025, registering a robust CAGR of over 35%. The market is projected to more than double by FY2030.

This significant growth is underpinned by the Government of India’s ambitious target to achieve 70% electrification of commercial vehicles and 40% of buses by 2030. Key national initiatives such as FAME-II, PM E-DRIVE, and the PLI-ACC scheme are accelerating this transition. India’s commercial electrification drive is reshaping logistics, public transport, and last-mile delivery segments through fleet modernization, cost efficiency, and sustainability imperatives.

India eCVs Market Growth Driven by Government and Rising Demand

-

Policy Push and Incentives: The India Electric Commercial Vehicles Market continues to gain momentum with strong government support through FAME-II, PM E-DRIVE (INR 10,900 crore), and PLI-ACC (INR 18,100 crore) schemes promote fleet electrification, domestic battery manufacturing, and charging network expansion.

-

Economic Viability: The India eCV market is increasingly supported by favorable cost dynamics. Electric buses operate at a significantly lower cost of INR 45–60 per km, compared to diesel buses at around INR 75 per km. In addition, reduced maintenance expenses are key motivators for fleet operators.

-

Rising Urban Logistics Demand: The surge in e-commerce and same-day delivery models has fueled the rapid deployment of electric two-wheelers (e-2Ws) and electric three-wheelers (e-3Ws) for hyperlocal and last-mile delivery.

-

Technology Advancements: Battery pack prices have declined from USD 159/kWh in 2022 to USD 95/kWh in 2025, boosting affordability and scaling adoption in LCVs and small fleets.

%20Market%20Insights.png)

Looking for a Section from Report? Start your Partial Purchase Request

Recent Developments and Investments in India eCVs Market

-

SPMEPCI, 2025: Under the Scheme to Promote Manufacturing of Electric Passenger Cars in India (SPMEPCI) 2025, the Government of India has reduced import duties on electric vehicles from 110% to 15% as of 2025.

-

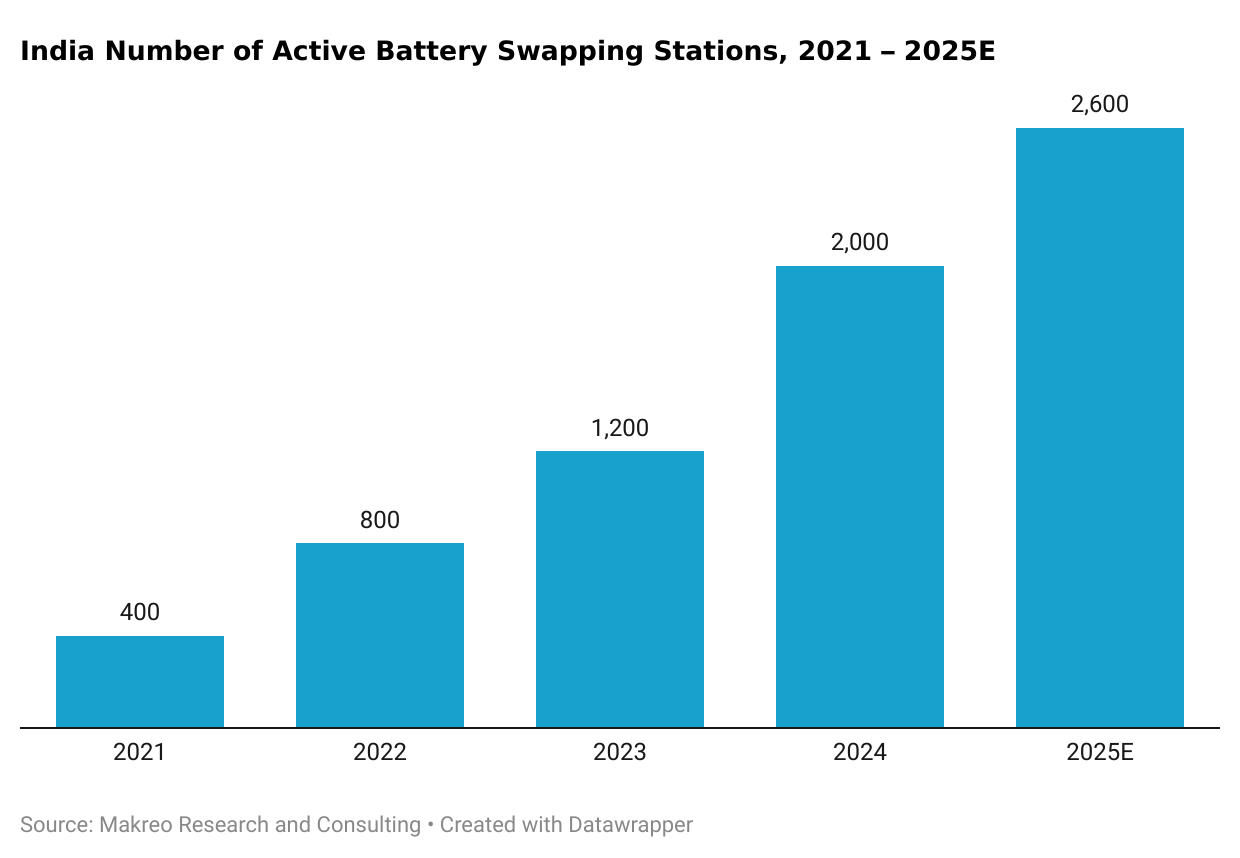

Battery Smart: The company surpassed 125,000 daily battery swaps for electric vehicles in 2025 and recorded over 50 million cumulative swaps. It conducted 3,456,000 battery swaps in May 2025.

Market Type of Vehicle Segmentation by Revenue, 2025E.png)

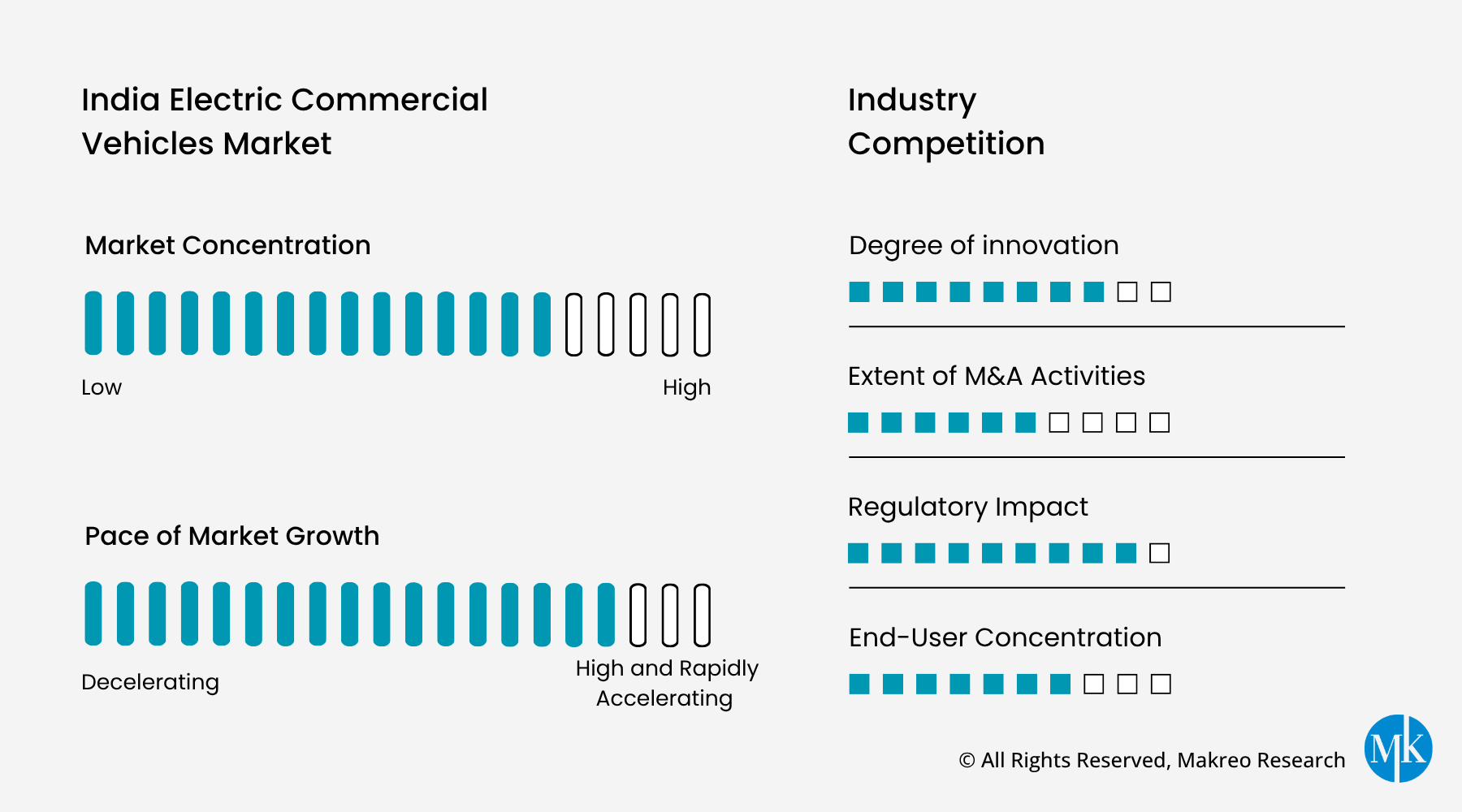

Electric Three-Wheelers Driving India’s Commercial Vehicle Electrification

Electric three-wheelers have become the cornerstone of India’s commercial vehicle electrification, leading adoption across both passenger mobility and goods transport segments. Their extensive use in urban mobility, shared transportation, and last-mile delivery logistics underscores their cost efficiency, operational flexibility, and strong adaptability to India’s dense urban networks. The segment continues to attract strong participation from fleet operators and OEMs alike, driving large-scale deployment of electric vehicles in daily commercial operations.

India Electric Commercial Vehicles Industry Insights

Market Revenue.png)

Steady Growth in India eCV Market Driven by Policy and Fleet Electrification

India’s Electric Commercial Vehicles (eCVs) market has recorded steady and sustained growth in recent years, supported by strong government initiatives, rapid fleet electrification, and rising adoption across logistics and public transport sectors. This growth has been primarily fueled by national programs such as FAME II, PLI-ACC, and PM E-DRIVE, which have encouraged OEM localization, reduced operating costs, and expanded charging and swapping infrastructure across major urban centers.

While the market remains in an early adoption stage for heavy commercial vehicles, strong momentum in three-wheelers, last-mile delivery fleets, and e-buses has established a resilient foundation for future expansion. With battery prices declining, import duties reduced, and major fleet operators committing to 100% electrification targets by 2030.

Scope of the Study for India Electric Commercial Vehicles Market

Makreo Research has released a comprehensive report titled "India Electric Commercial Vehicles (eCVs) Market and Forecast Report (2021–2030) – by Vehicle Type (2-Wheelers, 3-Wheelers, 4-Wheelers, Buses, Trucks), End Use (Logistics, Last-Mile Delivery), and Region Analysis", offering an in-depth assessment of India’s rapidly expanding commercial electric vehicle industry. The report provides a detailed overview of the market’s historical performance, current landscape, and future potential, highlighting key growth drivers such as:

-

Rising demand for fleet electrification across logistics, e-commerce, and public transport segments due to lower operational and maintenance costs.

-

Rapid expansion of charging and battery swapping infrastructure, supported by public–private partnerships and technological innovations.

-

Increasing participation of major OEMs and new entrants investing in localized production, battery innovation, and green fleet partnerships with leading corporates.

India Electric Commercial Vehicles Market Competitive Landscape and Leading OEM Analysis

This section offers an in-depth assessment of the competitive landscape within the India Electric Commercial Vehicles (eCVs) Market, providing detailed insights into the operational strengths, product strategies, and market positioning of leading manufacturers. The analysis compares major OEMs based on parameters such as market share, product portfolio diversity, production capacity, regional presence, and technological advancements, supported by detailed company profiles. Each profile outlines the following key aspects:

-

Product range and vehicle categories offered across electric commercial vehicles

-

Technological innovation and R&D capabilities

-

Strategic partnerships and collaborations with logistics operators, fleet service providers, and government agencies.

-

Recent business developments, such as fleet deployment contracts, order wins, capacity expansions, investment rounds, and key financial indicators.

Future Outlook and Growth Insights for India eCVs Market

The India Electric Commercial Vehicles (eCVs) Market is evolving from pilot-scale adoption to large-scale deployment, primarily driven by the logistics and public transportation sectors. Rapid cost declines, local battery production, and city-level clean mobility mandates will fuel continued double-digit growth.

The market’s future value is projected to be driven by aggressive fleet targets, infrastructure investment, and rising consumer awareness toward sustainable operations.

-

FY’2021 – FY’2025: Past and Present Scenario

-

FY’2025: Base year of study

-

FY’2025– FY’2030: Future Outlook

India Electric Commercial Vehicles Market Segmentation

-

2-Wheelers

-

3-Wheelers

-

4-Wheelers

-

Buses

-

Trucks

-

Logistics

-

Last-Mile Delivery

Geography Assessed

-

North

-

South

-

West

-

East

-

Competition

-

Mergers, Acquisitions, and Investments

-

Company Profiles

Tata Motors Commercial Vehicle Business Demerger: TML Commercial Vehicles Limited (TMLCV) was launched as a new entity on October 1, 2025, through a demerger of Tata Motors commercial vehicles business.

Ashok Leyland Consolidates Control Over Switch Mobility: In 2025, Ashok Leyland announced that its UK-based subsidiary, Optare PLC, increased its ownership in Switch Mobility Ltd to nearly 100%, consolidating its control over the electric vehicle arm.

Mahindra Last Mile Mobility Introduces Battery-as-a-Service Model: In 2025, Mahindra Last Mile Mobility Limited (MLMML) partnered with Vidyut to launch a Battery-as-a-Service (BaaS) model for its electric 3- and 4-wheelers. The plan lets customers rent batteries starting at INR 2.50 per km.

Companies Covered in the India eCVs Market

-

Tata Motors Limited

-

Switch Mobility Automotive Limited

-

Mahindra Last Mile Mobility Limited

-

Olectra GreenTech Limited

There are 12 players covered in this report. To know more, please reach out to sales@makreo.com

Table of Contents

- 1.Research Methodology

- 1.1.Research Objective

- 1.2.Research Design and Procedure

- 1.3.Research Methodology

- 1.4.Analytical Framework

- 2.India Commercial Vehicle (CV) Market – An Overview

- 2.1.India Commercial Vehicle (CV) Production and Sales

- 2.2.India Commercial Vehicle (CV) Production and Sales by Gross Weight

- 2.3.India Commercial Vehicle (CV) Sales by Fuel

- 3.India Electric Commercial Vehicles (eCVs) Market - Production and Sales

- 3.1.India Electric Commercial Vehicles (eCVs) Average Price

- 3.2.India Electric Commercial Vehicles (eCVs) Sales by Volume

- 3.3.India Electric Commercial Vehicles (eCVs) Sales by Value

- 4.India Electric Commercial Vehicles (eCVs) Market – Regional Trends

- 4.1.India Electric Commercial Vehicles (eCVs) Adoption by States

- 4.2.India Electric Vehicles Volume Sales by States

- 4.3.India Electric Commercial Vehicles (eCVs) Penetration by Top 3 States

- 4.4.India Electric Vehicle (EV) Sales by States

- 4.5.India Electric Vehicle (EV) Segment Wise Sales by Top States

- 4.6.India Electric Vehicle (EV) Sales by Top States

- 4.7.India Electric Bus Sales by Cities

- 4.8.India e-3W L5 Passenger Sales by Cities

- 4.9.India e-3W L5 Goods Sales by Cities

- 4.10.India e-4W Goods Carrier Sales by Cities

- 5.India Electric Commercial Vehicles (eCVs) Market - Trade

- 6.India Electric Commercial Vehicles (eCVs) Market Past and Present Performance

- 6.1.India Electric Commercial Vehicles (eCVs) Market - An Overview

- 6.2.India Electric Commercial Vehicles (eCVs) Market Past and Present Performance

- 7.India Electric Commercial Vehicles (eCVs) Market Segmentation

- 7.1.India Electric Commercial Vehicles (eCVs) Market Segmentation

- 7.1.1.India Electric Commercial Vehicles (eCVs) Market Type of Vehicle Segmentation by Revenue

- 7.1.2.India Electric Commercial Vehicles (eCVs) Market Type of Vehicle Segmentation by Volume

- 7.1.3.India Electric Commercial Vehicles (eCVs) Market Segmentation by Region

- 7.1.4.India Electric Commercial Vehicles (eCVs) Market Segmentation by End Use

- 7.1.India Electric Commercial Vehicles (eCVs) Market Segmentation

- 8.India Electric Commercial Vehicles (eCVs) Market - Challenges

- 9.India Electric Commercial Vehicles (eCVs) Market - Opportunities

- 10.India Electric Commercial Vehicles (eCVs) Market Future Outlook (2025–2030)

- 10.1.India Electric Commercial Vehicles (eCVs) Market Future Outlook

- 10.2.India Electric Commercial Vehicles (eCVs) Market Scenario Analysis

- 11.India Electric Commercial Vehicles (eCVs) Market Competitive Landscape

- 11.1.India Electric Commercial Vehicles (eCVs) Market Key Players by Market Share

- 11.2.India Electric Commercial Vehicles (eCVs) Market Key Players Product Portfolio

- 11.3.India Electric Commercial Vehicles (eCVs) Market Technology Innovations

- 11.4.India Last Mile Electric Commercial Fleet Comparison

- 12.India Electric Commercial Vehicles (eCVs) Market Company Profiles

- Company 1

- Business Overview

- Company 1 - Company Timeline

- Company 1 - Business Highlights

- Company 1 - Business Financials

- Company 2

- Business Overview

- Business Highlights

- Business Financials

- Company 3

- Business Overview

- Business Highlights

- Business Financials

- Company 4

- Business Overview

- R&D and Innovations

- Asset Security and Lending Structure

- Business Highlights

- Business Financials

- eCV Sales & Orders Summary

- Business Outlook

- Company 5

- Business Overview

- Business Highlights

- Business Financials

- Company 6

- Business Overview

- Business Highlights

- Business Financials

- Company 7

- Business Overview

- Business Highlights

- Business Financials

- Company 8

- Business Overview

- Business Highlights

- Business Financials

- Company 9

- Business Overview

- Business Highlights

- Business Financials

- Company 10

- Business Overview

- Business Highlights

- Business Financials

- Company 11

- Business Overview

- Business Highlights

- Business Financials

- Company 12

- Business Overview

- Business Highlights

- Business Financials

- Limitations of the Study

Related Reports — Automotive & Transportation