Egypt Freight Market Size and Forecast (2021–2030) – Analysis by Mode of Transportation (Road, Rail, Marine, Air), Freight Type, Shipment Category, Trade Corridors, Industry Verticals, and Service Providers

Egypt Freight and Logistics Market Size

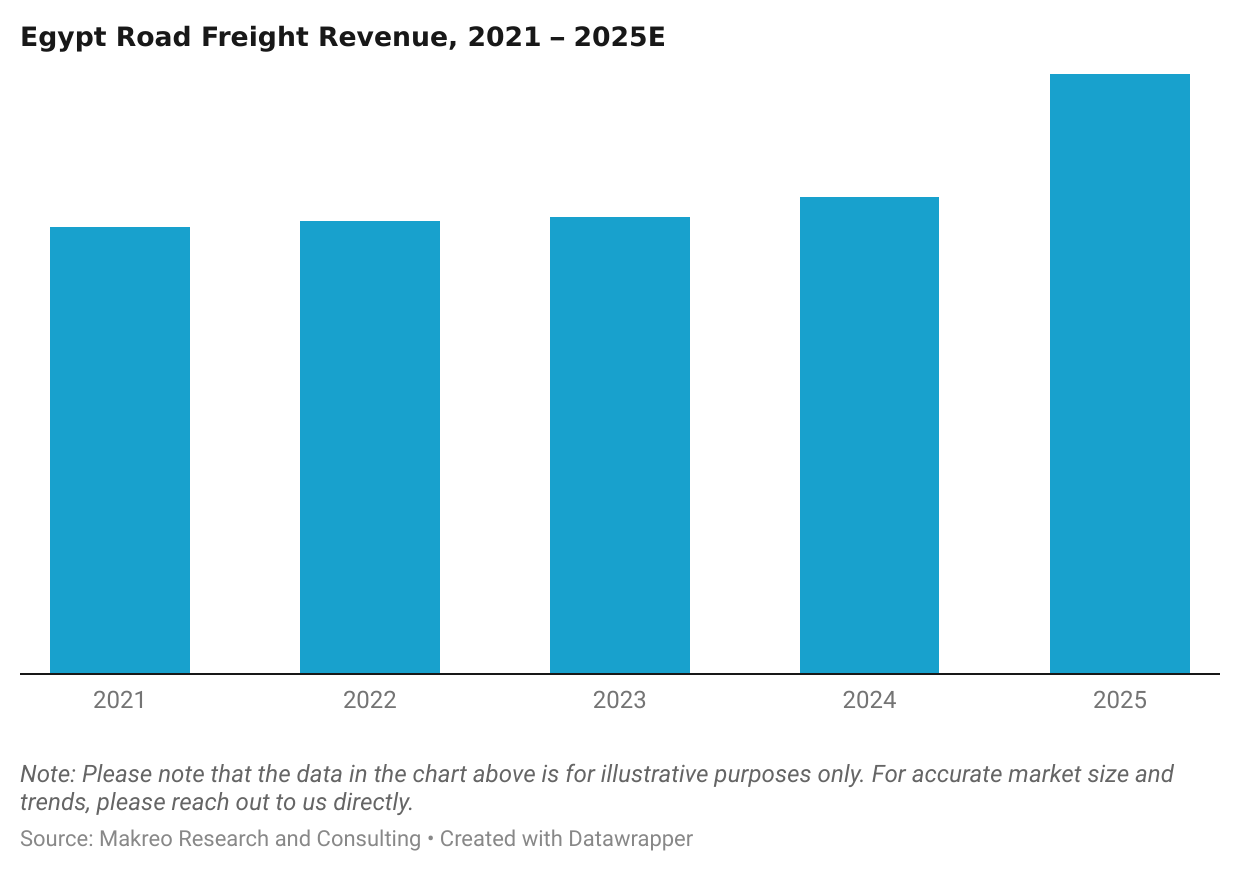

Egypt’s Freight and Logistics Market has experienced mixed growth in recent years, recording a CAGR of just over 2% between 2021 and 2025. This modest growth reflects broader economic fluctuations, policy shifts, and recurring global trade disruptions. These dynamics have shaped freight demand patterns across key transport corridors and industry segments.

Within maritime logistics, the Suez Canal Authority (SCA) reported consistent revenue growth from USD 6.33 billion in 2021 to a record USD 9.40 billion in 2023. However, revenues dropped sharply to USD 3.99 billion in 2024, driven by geopolitical tensions and disruptions affecting Red Sea and Bab al-Mandeb shipping lanes, including heightened conflict-related risks linked to the U.S., Israel, and Yemeni Houthi activities.

-

Agriculture, manufacturing, construction, wholesale & retail trade, and oil & gas collectively contribute around 85% of Egypt’s total freight demand in 2024.

-

This distribution highlights the underlying structure of Egypt’s goods economy, where bulk commodity flows (agriculture, construction materials) and industrial cargoes (manufactured goods, petrochemicals) account for most transported volume.

Looking for a Section from Report? Start your Partial Purchase Request

Egypt Freight Industry Insights

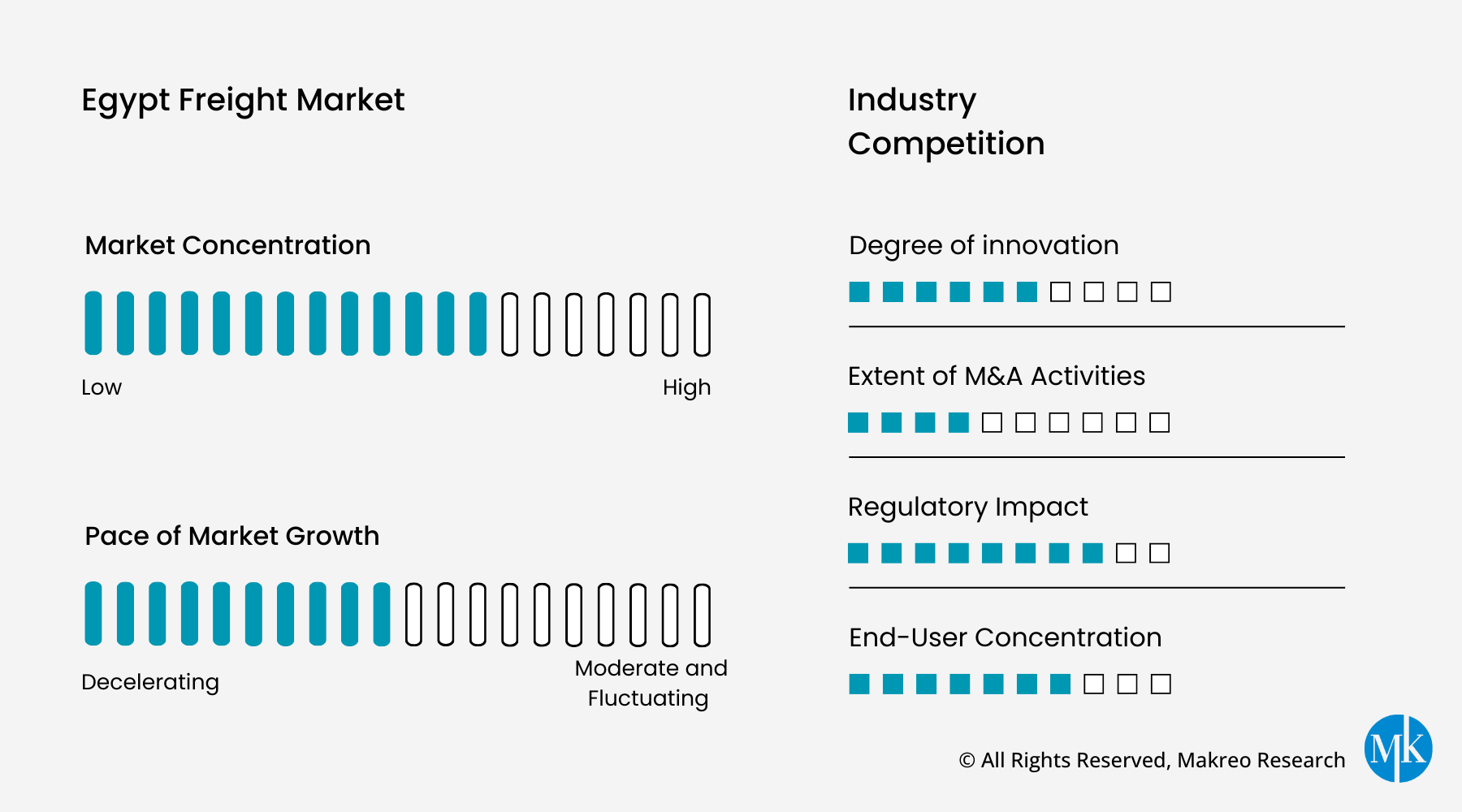

Competitive Landscape of the Egypt Freight Market

This section provides a comparative analysis of major players in Egypt’s freight and logistics market, assessing them across key parameters such as capacity, service portfolio, pricing, technology adoption, and regional presence. It highlights each company’s strategic direction, infrastructure investments, service innovations, and market positioning within Egypt’s freight ecosystem. The section also reviews competitive strategies, including collaborations, digitalization initiatives, and multimodal partnerships, along with funding trends, mergers, and public–private projects driving growth in Egypt’s freight market.

M&A, Investments, and Funding Activity in the Egypt Freight Market

This section reviews the recent mergers, acquisitions, and investments of the companies listed below, along with the latest funding trends in the market.

-

Egypt’s strategic maritime position, located at the crossroads of Africa, Asia, and Europe, with access to the Mediterranean Sea and the Red Sea, makes it one of the most important global maritime hubs.

-

The country manages over 2,000 km of coastline and operates ~15 commercial seaports, including six Mediterranean (Alexandria, Damietta, Port Said, Dekheila, El-Arish, and Abu Qir) and nine Red Sea ports (Sokhna, Adabiya, Safaga, Nuweiba, Suez, Sharm El-Sheikh, Hurghada, Al-Tor, and Berenice).

-

The Suez Canal is Egypt’s most valuable maritime asset, a global chokepoint for trade, linking the Red Sea to the Mediterranean and handling ~12% of global maritime trade.

Fleet Size and Structure

According to data from the Central Agency for Public Mobilization and Statistics (CAPMAS, 2023–2024), Egypt’s licensed commercial truck fleet is estimated at 1.2–1.3 million vehicles, making it one of the largest in North Africa. The fleet has expanded significantly since 2020, reflecting rising logistics demand and government-led infrastructure development.

Sectoral Distribution

Earlier figures from the Federation of Egyptian Industries (FEI) and the Ministry of Transport indicated that public business sector companies collectively owned 1,588 trucks, with a total capacity of around 5,480 million ton-km. In contrast, the private sector now accounts for over 99% of the country’s road freight operations, with the public sector representing less than 0.2% of national capacity.

Operational and Capacity Constraints in Egypt’s Rail Freight Network

-

The national rail network is about 5,100 km in length (broad gauge) and ~60% of the network is concentrated in the Nile Delta and Nile Valley corridors.

-

In general, freight trains operate at a lower speed than trucks; more so, several passenger trains (on main lines, as well as branch lines such as Banha-Port Said-Tanta-Damietta) are slow.

-

Freight cars operate at a low load factor, and freight car cycle time, length of time consumed by a freight car from one loading to the next again, reaches 14 days on average.

Segmental Revenue, H1 2024 & H1 2025.png)

-

Middle East Investment Strategy: DHL Group announced a long-term regional expansion plan committing over EUR 500 million between 2024 and 2030. The investment will be distributed across DHL’s Express, Freight Forwarding, Supply Chain, and eCommerce divisions, with a strategic focus on accelerating growth in key Gulf markets, including Saudi Arabia and the United Arab Emirates.

-

Sustainable Fleet Expansion Initiative: In March 2025, DHL Supply Chain, in partnership with Scania, introduced 25 Euro 5 biodiesel-powered trucks to enhance fuel efficiency and reduce emissions within its road transport operations.

-

SME Export Support Program in Zimbabwe: In February 2025, Old Mutual Zimbabwe’s Eight2Five Innovation Hub partnered with DHL GoTrade to support small businesses seeking to expand into export markets. The initiative—Trade and Grow Beyond Borders—aims to equip 300 SMEs and startups with the tools, training, and resources needed to participate in global trade.

Key Investments and Expansion Activities in Egypt’s Logistics Market

-

Safaga Integrated Logistics Center – Beit Logistics: Beit Logistics has signed a land-use agreement with the Golden Triangle Economic Zone Authority to develop an integrated logistics facility in Safaga valued at EGP 500 million. The planned 15-feddan site will include advanced warehousing infrastructure, container handling capabilities, and a green transport fleet, supporting increased logistics efficiency and strengthening Egypt’s Red Sea trade capacity.

-

Growth Outlook from Egyptian Global Logistics (EGL): Egyptian Global Logistics (EGL) highlighted a positive growth trajectory for the country's logistics and warehousing sector, estimating its value at USD 31.7 billion in 2024. The company anticipates continued expansion driven by rising trade flows and large-scale infrastructure development, contributing to accelerating investment in warehousing and logistics facilities across Egypt.

East Port Said Industrial Zone - Strategic Infrastructure and Development Overview

-

The East Port Said (EPS) Industrial Zone spans approximately 63 km² and forms part of the broader East Port Said Integrated Development, which integrates industrial, logistics, and port infrastructure. The zone is strategically located 20 km from Port Said City and 200 km from Cairo.

-

The development includes dedicated utilities infrastructure, featuring a 150,000 m³/day desalination facility and a 100,000 m³/day wastewater treatment plant, along with logistics service clusters supporting warehousing, container handling, and value-added operations within the hinterland.

-

The master plan includes capacity for approximately 1,200 factories across large, medium, and small industrial segments, with the objective of creating around 100,000 direct and indirect jobs.

-

EPS is designed to function as a major transshipment and trade gateway, connecting Europe, East Africa, and the Middle East through its proximity to the Suez Canal corridor.

-

The development plan also includes the establishment of Al-Salam City, a residential zone intended to accommodate up to one million inhabitants.

-

Expected to generate over 80,000 job opportunities upon completion.

Scope of the Study for Egypt Freight Market

Makreo Research has released a comprehensive study titled, "Egypt Freight Market Size and Forecast (2021–2030) – Analysis by Mode of Transportation (Road, Rail, Marine, Air), Freight Type, Shipment Category, Trade Corridors, Industry Verticals, and Service Providers", examines Egypt’s freight and logistics sector in the context of modernization, industrial expansion, and shifting global trade dynamics. It positions Egypt as a strategic logistics hub connecting Africa, the Middle East, and Europe.

Modal Breakdown of the Egypt Freight Market

The study assesses the performance of Egypt’s key transportation modes, providing market size, throughput, and revenue trends.

-

Road freight: Dominant in domestic cargo.

-

Rail freight: Gradual improvements supported by infrastructure upgrades.

-

Marine freight: Driven by port modernization and Suez Canal activity.

-

Air freight: Strengthening due to government and private investments.

Each mode is evaluated based on capacity, operational efficiency, and connectivity across major national and cross-border trade corridors.

Suez Canal and SCZone Analysis in the Egypt Freight Market

A major section tracks:

-

Vessel movements

-

Cargo tonnage handled

-

Revenue trends

-

Impact of Red Sea disruptions

-

Ongoing expansions and modernization initiatives

The analysis further extends to the Suez Canal Economic Zone (SCZone), evaluating its industrial zones and their role in strengthening manufacturing activity, re-export flows, and the overall trade competitiveness.

Port Performance and Infrastructure

The report evaluates the performance of key ports:

-

Alexandria Port

-

Port Said

-

Damietta Port

-

Red Sea Ports

Coverage includes infrastructure expansion, modernization projects, operational efficiency improvements, and throughput metrics that strengthen Egypt’s position as a growing transshipment hub.

Domestic Freight Network Assessment

This section examines the structure and performance of Egypt’s domestic freight network across road, rail, and air transport systems, with focus on:

-

Road network dominance

-

Efforts to modernize rail freight

-

Expansion of air cargo capacity and facilities

-

Integration of multimodal logistics infrastructure

Competitive Landscape of the Egypt Freight Market

The report provides a structured assessment of major logistics and freight companies, profiling:

-

Business strategies

-

Market positioning

-

Key investments

-

Mergers and acquisitions

-

Service provider ecosystem

Egypt Freight and Logistics Market Outlook and Forecast

The concluding section provides a forward-looking revenue outlook for the Egypt Freight Market Outlook, including:

-

Policy reforms

-

Infrastructure pipeline

-

Macroeconomic indicators

-

Trade growth trajectories

-

Multimodal connectivity improvements

-

2021 - 2025: Past and Present Scenario

-

2025: Base year of study

-

2026 - 2030: Future Outlook

Egypt Freight Market Segmentation

-

Road Freight

-

Rail Freight

-

Marine Freight (Sea Cargo)

-

Air Freight

-

Domestic Freight

-

International Freight

-

Containerized Cargo

-

Bulk Cargo (Dry and Liquid)

-

Break Bulk

-

Perishables

-

Express and High-Value Goods

Geography Assessed

-

Mediterranean Corridor (Alexandria–Cairo)

-

Port Said Cluster (East & West Port Said / Transshipment)

-

Damietta Port Corridor

-

Red Sea Corridor (Ain Sokhna–Suez–Safaga)

-

Suez Canal Economic Zone (SCZone)

-

Agriculture

-

Manufacturing

-

Construction

-

Wholesale & Retail Trade

-

Oil & Gas

-

Public Sector Entities (Egyptian National Railways, Port Authorities)

-

Private Logistics Operators

-

Freight Forwarders

-

Public–Private Partnership (PPP) Operators

Future Outlook and Strategic Insights for the Egypt Freight Market

Egypt’s freight market is positioned for steady growth, supported by major port expansion initiatives, continued activity within the SCZONE, and sustained investment across road, rail, and air logistics infrastructure. Although short-term performance continues to feel the impact of Red Sea geopolitical tensions, elevated logistics costs, and operational bottlenecks, the medium-term outlook remains strong. Enhanced multimodal connectivity, upgraded port infrastructure, and targeted policy reforms are expected to drive efficiency and competitiveness. With a projected CAGR of 8.32% between 2025E and 2030F, growth will be underpinned by increasing freight activity across manufacturing, construction, and agriculture, alongside a recovery in Suez Canal revenue flows. Collectively, these factors reinforce Egypt’s role as an emerging logistics gateway with expanding opportunities across maritime, road, and integrated freight services.

Companies Covered in the Egypt Freight Market

-

DHL Global Forwarding Egypt S.A.E.

-

Agility Logistics Egypt S.A.E.

-

Aramex PJSC, Schenker Egypt LLC

There are 9 players covered in this report. To know more, please reach out to sales@makreo.com.

Table of Contents

- 1.Research Methodology

- 1.1.Objective of the Study

- 1.2.Market Definitions and Key Terminologies

- 1.3.Research Design and Procedure

- 1.4.Research Methodology

- 1.5.Data Collection Methods

- 2.Egypt Freight Market Past and Present Performance and Modal Analysis

- 2.1.Egypt Freight Market Past and Present Performance

- 2.1.1.Egypt Freight Market by Different Modes Past and Present Performance

- 2.1.1.1.Egypt Freight Transportation Domestic and International Mode of Transport

- 2.1.2.Egypt Freight Share by Geography / Trade Corridor

- 2.1.3.Egypt Freight Transport and Port Performance Analysis

- 2.1.1.Egypt Freight Market by Different Modes Past and Present Performance

- 2.2.Egypt Freight Market by Key Industry Demand

- 2.3.Egypt Freight Market – Demand and Supply Side Insights

- 2.1.Egypt Freight Market Past and Present Performance

- 3.Analysis of Suez Canal Performance and Strategic Outlook

- 4.Major Industrial Zones within the Suez Canal Economic Zone (SCZONE)

- 4.1.Egypt Industrial Zones Overview

- 4.2.Key Industrial Zones under Suez Canal Economic Zone (SCZONE)

- 5.Egypt Major Ports Infrastructure Development, Expansion, and Performance Overview

- 6.Egypt Maritime Transport and Port Operations Overview

- 6.1.Egypt Marine Cargo Overview

- 6.2.Egypt Traffic at Different Seaports

- 6.3.Egypt Maritime Cargo and Vessel Handling Statistics

- 6.3.1.Egypt Vessel Traffic and Port Comparison

- 7.Egypt Road Freight Analysis

- 7.1.Egypt Road Freight Overview

- 7.1.1.Egypt Road Freight Fleet Overview

- 7.1.2.Egypt Road Freight Volume and Revenue Outlook

- 7.1.Egypt Road Freight Overview

- 8.Egypt Air Cargo Analysis

- 8.1.Egypt Air Cargo Overview

- 8.2.Egypt Air Cargo Revenue

- 9.Egypt Rail Freight Analysis

- 9.1.Egypt Rail Freight Overview

- 9.1.1.Egypt Rail Freight Volume and Revenue

- 9.1.Egypt Rail Freight Overview

- 10.Egypt Freight Market Competition

- 10.1.Egypt Freight Market Key Players Overall Performance Scorecard

- 10.2.Egypt Freight Market Key Players by Mode of Coverage

- 10.3.Egypt Freight Market Key Players by Innovation

- 10.4.Egypt Freight Market Key Players Turn-around Times (TT)

- 10.5.Egypt Freight Market Top Digital Freight Platforms and Compliance Certifications

- 10.6.Egypt Freight Market Key Players by Network Coverage (Industrial Zones and Ports)

- 10.7.Egypt Freight Market Key Startup Players

- 11.Egypt Freight Market Company Profiles

- 11.1.Player 1- Business Overview

- Business Highlights

- Business Financials

- 11.2.Player 2 - Business Overview

- Business Highlights

- Business Financials

- 11.3.Player 3 - Business Overview

- Business Highlights

- Business Financials

- 11.4.Player 4 - Business Overview

- Business Highlights

- Business Financials

- 11.5.Player 5 - Business Overview

- Business Highlights

- Business Financials

- 11.6.Player 6 - Business Overview

- Business Highlights

- Business Financials

- 11.7.Player 7 - Business Overview

- Business Highlights

- Business Financials

- 11.8.Player 8 - Business Overview

- Business Highlights

- Business Financials

- 11.9.Player 9 - Business Overview

- Business Highlights

- Business Financials

- 11.10.Player 10 - Business Overview

- Business Highlights

- Business Financials

- 12.Egypt Freight Market Challenges

- 13.Egypt Freight Market Future Outlook and Opportunities

- Limitations of the Study

Related Reports — Automotive & Transportation