India Solar Photovoltaic (PV) Market Size and Forecast (2021-2030) - Analysis by Application, Deployment Model, Grid Type, and Components

India Solar Photovoltaic (PV) Market Size

India’s Solar Photovoltaic (PV) market has recorded strong and sustained expansion, registering a CAGR of 12.66% between 2021 and 2025, and is expected to continue expanding strongly through the end of the decade. This growth is underpinned by India’s rapid capacity additions in utility-scale and rooftop solar sector. Market growth is further underpinned by a supportive policy framework, including the India Solar PLI Scheme, ALMM, PM-KUSUM Scheme, and Green Open Access regulations, and a sharp scale-up in domestic manufacturing across modules, cells, and upstream components. Rising power demand, declining solar tariffs, and increasing emphasis on energy security and decarbonization are accelerating solar adoption across residential, commercial & industrial, and utility segments, positioning solar PV as a central pillar of India’s clean energy transition and long-term power mix.

India Solar Photovoltaic (PV) Market Growth Drivers

-

The India Solar Photovoltaic (PV) Market is experiencing accelerated growth, supported by a strong policy framework that includes the Production Linked Incentive (PLI) Scheme, Approved List of Models and Manufacturers (ALMM), Basic Customs Duty (BCD), Green Open Access Rules, and the PM-KUSUM Scheme. These have strengthened domestic manufacturing, reduced import dependence, and improved project bankability and investor confidence.

-

A rapidly expanding domestic solar manufacturing ecosystem is enhancing India’s self-reliance across the PV value chain, with significant capacity additions in modules, cells, wafers, and polysilicon. Indian manufacturers are increasingly adopting advanced technologies such as Mono-PERC, TOPCon, HJT, and bifacial modules, scaling R&D capabilities, and expanding export footprints.

-

Deployment of advanced solar technologies is gaining strong traction. Increased adoption of high-efficiency modules, digital monitoring systems, grid-connected and off-grid solutions, along with declining system costs and improved grid integration, is accelerating solar penetration across residential, commercial & industrial, and government segments, reinforcing solar PV’s role in India’s energy transition.

Scope of the Study for India Solar Photovoltaic (PV) Market

Makreo Research has released a comprehensive report titled "India Solar Photovoltaic (PV) Market Size and Forecast (2021-2030) - Analysis by Application, Deployment Model, Grid Type, and Components", The report provides an in-depth evaluation of India’s rapidly expanding solar energy ecosystem, examining market structure, growth dynamics, and competitive positioning across key segments of the India Solar PV Market.

The study opens with a structured assessment of the India Solar Photovoltaic (PV) Market, analysing historical performance, current market conditions, and forward-looking indicators to define the sector’s overall growth trajectory.

India Solar PV Capacity Expansion and Demand Drivers

India’s Solar Photovoltaic (PV) Market is experiencing accelerated capacity expansion across utility-scale, rooftop, and off-grid segments, driven by:

-

Declining solar tariffs

-

Rising electricity demand

-

Long-term national renewable energy targets

Policy and Regulatory Environment

The market benefits from strong policy and regulatory support, including:

-

The Production Linked Incentive (PLI) scheme for advanced solar manufacturing

-

Flagship government initiatives such as PM-KUSUM

-

Large-scale solar park development programs

India Solar PV Manufacturing Growth

Domestic solar manufacturing is expanding rapidly, supported by increasing investments in high-efficiency PV technologies, including:

-

Mono-PERC

-

TOPCon

-

HJT

-

Bifacial modules

-

Capacity expansion across the value chain

Company Profiles of Leading Players in the India Solar PV Market

This section provides a comprehensive assessment of the competitive landscape of India’s Solar Photovoltaic (PV) market, highlighting the operational scale, manufacturing capabilities, and strategic positioning of leading domestic players across the solar value chain.

Company Benchmarking and Comparative Analysis

The study presents a comparative evaluation of major companies based on key competitive parameters, including:

-

Manufacturing capacity

-

Technology adoption

-

Project portfolio and execution capabilities

-

Geographic presence

-

Market share across utility-scale, rooftop, and manufacturing segments

Value Chain Coverage and Market Segmentation

The analysis captures company participation across different solar PV value chain segments, assessing positioning in:

-

Utility-scale solar projects

-

Rooftop and distributed solar

-

Solar module, cell, and integrated manufacturing

Detailed Company Profile Framework

Each company profile provides an in-depth overview covering the following core aspects:

Technology and Product Portfolio

-

Technology focus (e.g., module types and efficiency levels)

-

Product mix across cells, modules, and systems

Capacity and Operational Capabilities

-

Installed and manufacturing capacities

-

Project execution and EPC capabilities

-

End-use market focus

Corporate Structure and Market Footprint

-

Ownership structure

-

Domestic and international geographic footprint

-

Export presence and strategic partnerships

Recent Developments and Financial Indicators

-

Capacity expansions and greenfield/brownfield projects

-

PLI scheme allocations and related investments

-

Key financial indicators and recent business developments

India Solar Photovoltaic (PV) Market Outlook and Strategic Insights

The report concludes with a forward-looking assessment of the India Solar Photovoltaic (PV) Market, outlining the key challenges and growth opportunities expected to influence the sector through 2030. It identifies strategic priorities for stakeholders, including scaling domestic manufacturing across the solar PV value chain, accelerating rooftop and commercial & industrial (C&I) adoption, strengthening grid infrastructure and storage integration, and advancing high-efficiency and next-generation solar technologies.

These insights are designed to inform investment decision-making, policy development, and long-term strategic planning, reinforcing India’s expanding role in global solar energy deployment and manufacturing.

-

2021 - 2025: Past and Present Scenario

-

2025: Base year of study

-

2026 - 2030: Outlook

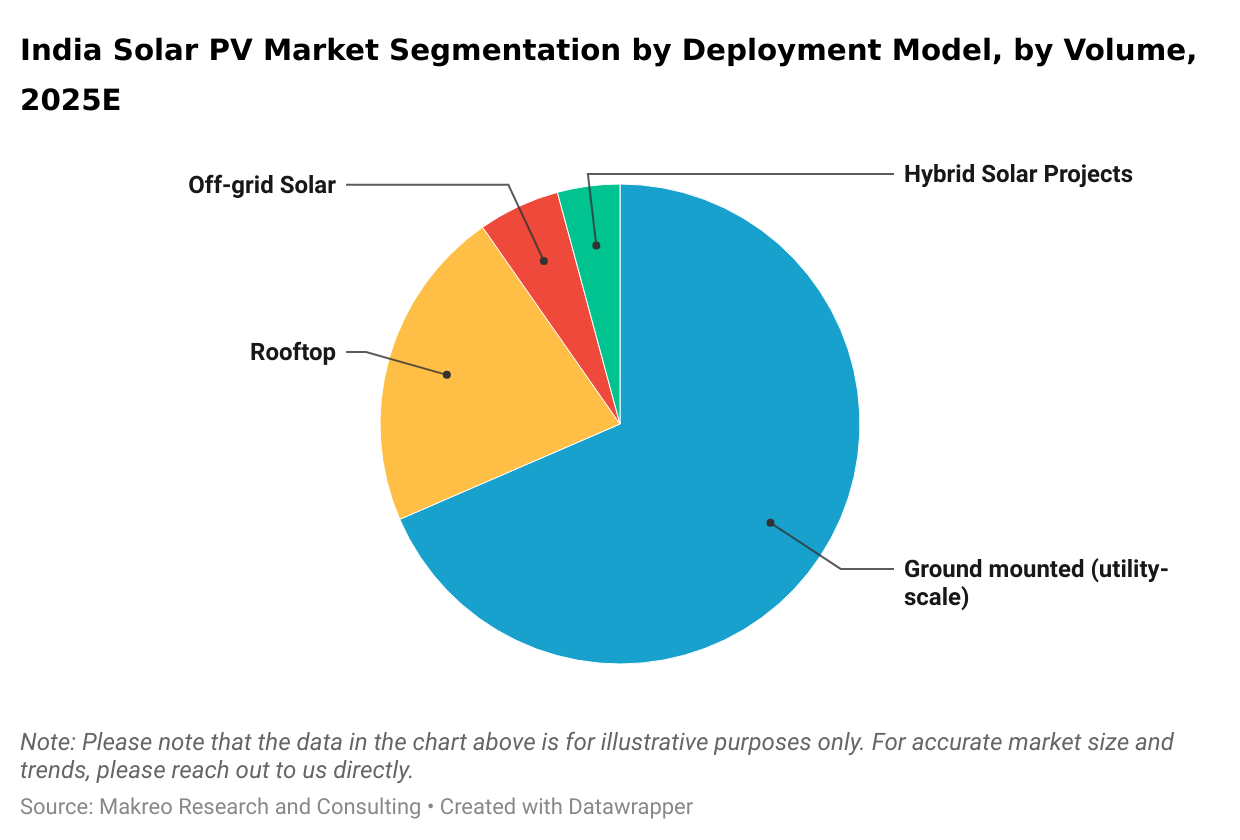

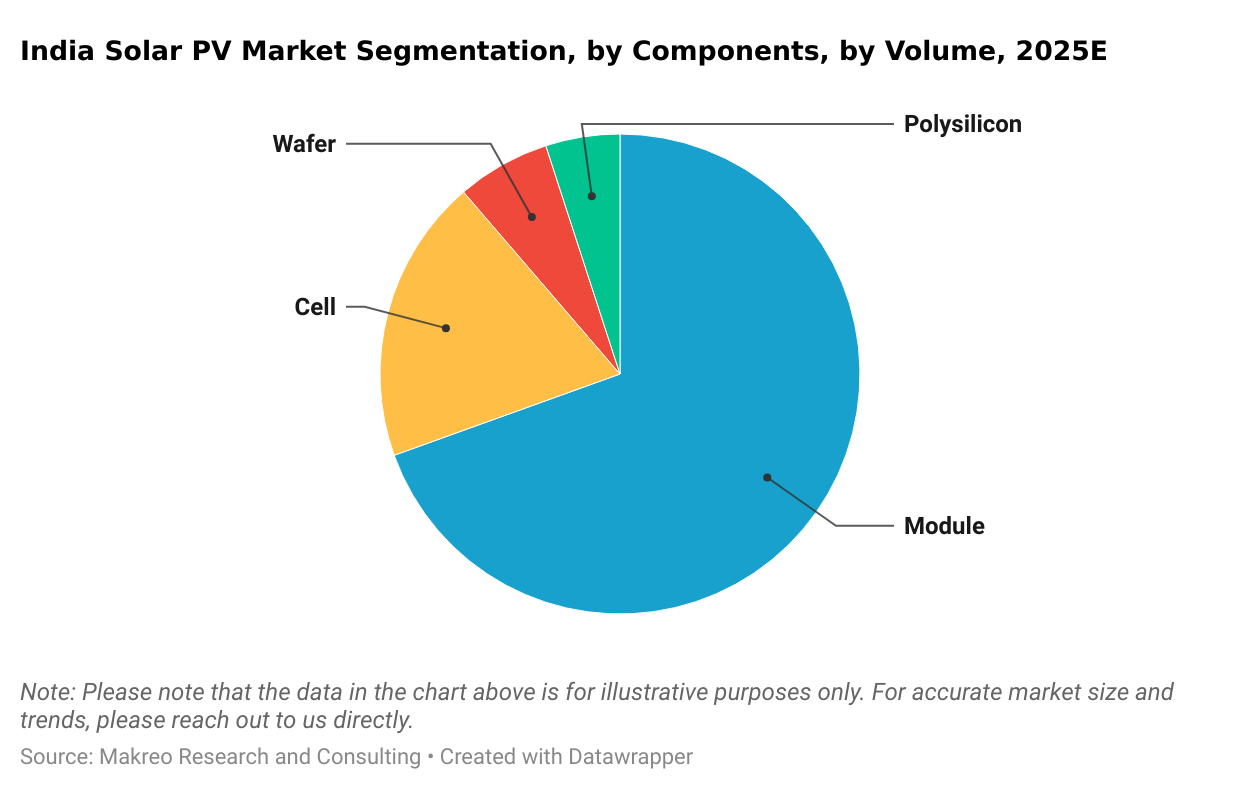

India Solar PV Market Segmentation

-

Residential

-

Commercial & Industrial

-

Government Buildings

-

Ground Mounted (utility-scale)

-

Rooftop

-

Hybrid Solar Projects

-

Off-grid Solar

-

On Grid

-

Off Grid

-

Module

-

Cell

-

Wafer

-

Polysilicon

-

Competition

-

Mergers, Acquisitions, and Investments

-

Funding Timeline

-

Company Profiles

India Solar PV Market Growth Driven by Policy Support and Capacity Expansion

India’s Solar Photovoltaic (PV) market has exhibited strong and consistent growth in recent years, supported by large-scale capacity additions, declining solar tariffs, and sustained regulatory support. While the market during 2021–2024 was marked by supply-chain disruptions, rising input costs, and adjustments to new policy frameworks such as BCD and ALMM, these transitional challenges were offset by accelerating domestic manufacturing, growing investor confidence, and increasing demand across utility-scale and rooftop segments. Continued investments in high-efficiency PV technologies, grid integration, and domestic supply-chain strengthening have positioned India for accelerated growth in the global solar energy ecosystem.

Recent Policy and Market Developments in India Solar PV Market

-

Expansion of Domestic Solar Manufacturing under PLI and ALMM: India accelerated domestic solar manufacturing capacity through the Production Linked Incentive (PLI) scheme and stricter enforcement of the Approved List of Models and Manufacturers (ALMM). Between FY2024 and FY2025, solar module manufacturing capacity nearly doubled, alongside sharp increases in solar cell capacity, reducing dependence on imported equipment.

-

Policy Measures Enhancing Project Viability and Market Access: Recent refinements to Basic Customs Duty (BCD), the rollout of Green Open Access Rules, and targeted incentives for rooftop and decentralized solar under schemes such as PM Surya Ghar and PM-KUSUM have improved project viability across residential, C&I, and utility-scale segments.

India Solar Photovoltaic Market Deployment Trends

In 2025, the India Solar Photovoltaic (PV) Market continues to be anchored by ground-mounted utility-scale projects, which continue to form the backbone of large-scale power generation due to their cost efficiency, faster execution, and strong grid integration. Rooftop solar installations are accounting for a steadily increasing share of capacity additions, supported by residential subsidy programs, rising demand from commercial and industrial users, and growing awareness of distributed energy solutions. Hybrid solar projects, combining solar with other renewable sources or storage, are gradually gaining traction to enhance grid stability and optimize land use, while off-grid solar systems continue to play a vital role in electrifying remote and underserved regions where grid access remains limited.

Recent Strategic Developments in the India Solar PV Market

-

Waaree’s Acquisition of Enel Green Power India (2025): In January 2025, Waaree signed an agreement to acquire 100% of EGP India for INR 792 crore. EGP India brings a renewable energy platform with ~640 MWAC (≈760 MWDC) of operational solar and wind projects and a project pipeline of ~2.5 GW across India.

-

RSWM–Adani Hybrid Power Partnership: In 2025, RSWM Limited signed strategic investment agreements with Adani Solar Energy Jodhpur Six Ltd and Adani Renewable Energy Forty-One Ltd to secure 60 MW of solar-wind hybrid power. As part of the deal, RSWM will acquire a minimum 26% equity stake in both project companies, ensuring long-term access to renewable energy for its operations.

-

Vikram Solar IPO and Capacity Expansion Strategy: In August 2025, Vikram Solar completed its initial public offering, priced between INR 315–332 per share, raised about INR 2,079 crore. It comprised a INR 1,500 crore fresh issue and a INR 579 crore OFS, with INR 621 crore secured from anchor investors. The IPO proceeds also support plans to scale up total module capacity to 10.50 GW by FY26 and 15.50 GW by FY27.

Companies Covered in the India Solar Photovoltaic Market

-

Waaree Energies Limited

-

Mundra Solar PV Ltd. (Adani Solar)

-

Vikram Solar Limited

There are 9 players covered in this report. To know more, please reach out to [email protected]

%20Market%20Growth.png)

Looking for a Section from Report? Start your Partial Purchase Request

Table of Contents

- 1.India Solar Photovoltaic (PV) Market Past and Present Performance

- 1.1.India Solar Photovoltaic (PV) Market - An Overview

- 1.2.Recent Developments in India Solar Photovoltaic (PV) Market

- 1.3.India Solar Photovoltaic (PV) Market Past and Present Performance

- 2.India Solar Photovoltaic (PV) Market Segmentation

- 2.1.India Solar Photovoltaic (PV) Market Segmentation Overview

- 2.1.1.India Solar Photovoltaic (PV) Market Segmentation by Deployment Model

- 2.1.2.India Solar Photovoltaic (PV) Market Segmentation by Application

- 2.1.3.India Solar Photovoltaic (PV) Market Segmentation by Components and Grid Type

- 2.1.India Solar Photovoltaic (PV) Market Segmentation Overview

- 3.India Solar Photovoltaic (PV) Market Regulatory Policies and Incentives

- 3.1.India Solar Photovoltaic (PV) Manufacturing & Residential Incentives

- 3.2.India Policy and Regulatory Framework for Solar Energy

- 3.3.India Solar Photovoltaic (PV) Market Key Initiatives

- 3.4.India PLI Program for Advanced Solar Photovoltaic (PV) Manufacturing

- 3.5.Major Investments and Capacity Additions in India Solar Photovoltaic (PV) Market

- 4.India Solar Photovoltaic (PV) Market Pricing Trends

- 5.India Solar Photovoltaic (PV) Market Capacity Assessment

- 5.1.India Solar Installed Capacity Growth and Cumulative Capacity Scenarios

- 5.2.India Rooftop Solar Capacity of India

- 5.3.India Ground Mounted Solar Capacity

- 5.4.India Solar Power Installation Trends, Renewable Share & Segmentation

- 5.5.India Solar Energy Capacity and Off-Grid Renewable Energy Deployment

- 5.6.India Solar Manufacturing Demand Projection

- 5.7.India Solar Energy Potential by Different States

- 6.India Solar Photovoltaic (PV) Market Competitive Landscape

- 6.1.India Solar Photovoltaic (PV) Market Top Players by Revenue

- 6.2.India Solar Photovoltaic (PV) Market Key Players by Business Segments

- 6.3.India Solar Photovoltaic (PV) Market Major Players by Manufacturing Capacity

- 6.4.India Solar Photovoltaic (PV) Market Major Players Key Capacities

- 6.5.India Solar Photovoltaic (PV) Key Players Future Capacity Expansion

- 7.India Solar Photovoltaic (PV) Market Mergers /Acquisitions/ Investments/ Divestments

- 7.1.Mergers /Acquisitions/ Investments/ Divestments

- 8.India Solar Photovoltaic (PV) Market Funding Timeline

- 8.1.Funding Timeline

- 9.India Solar Photovoltaic (PV) Market Company Profiles

- 9.1.Player 1 - Business Overview

- 9.1.1.Business Highlights

- 9.1.2.Operational Highlights

- 9.1.3.Business Financials

- 9.1.4.Manufacturing Milestones and Key Projects

- 9.2.Player 2 - Business Overview

- 9.2.1.Business Highlights

- 9.2.2.Business Financials

- 9.3.Player 3 - Business Overview

- 9.3.1.Business Highlights

- 9.3.2.Operational Highlights

- 9.3.3.Business Financials

- 9.4.Player 4 - Business Overview

- 9.4.1.Business Highlights

- 9.4.2.Business Financials

- 9.5.Player 5 - Business Overview

- 9.5.1.Business Highlights

- 9.5.2.Operational Highlights

- 9.5.3.Business Financials

- 9.6.Player 6 - Business Overview

- 9.6.1.Business Highlights

- 9.6.2.Operational Highlights

- 9.6.3.Business Financials

- 9.7.Player 7 - Business Overview

- 9.7.1.Business Highlights

- 9.7.2.Business Financials

- 9.8.Player 8 - Business Overview

- 9.8.1.Business Highlights

- 9.8.2.Business Financials

- 9.9.Player 9 - Business Overview

- 9.9.1.Business Highlights

- 9.9.2.Business Financials

- 9.1.Player 1 - Business Overview

- 10.India Solar Photovoltaic (PV) Market Challenges

- 11.India Solar Photovoltaic (PV) Market Opportunities

- 12.India Solar Photovoltaic (PV) Market Future Outlook

- Limitations of the Study

Related Reports - Energy and Utilities