Why Egypt’s Logistics Market Is Shifting From Capacity Expansion to Integration-Led Growth

Egypt’s logistics market is shifting to integration-led growth as ports, rail, dry ports, and the Suez Corridor reshape multimodal connectivity and trade flows.

From Transit Dependency to Integrated Infrastructure - How Ports, Rail, Dry Ports, and the Suez Corridor Are Repositioning Egypt’s Logistics Economy

Between 2021 and 2025, Egypt’s logistics, warehousing, and cold chain market expanded by more than USD 3 billion in incremental revenue, driven by rising port throughput, accelerating domestic freight demand, and gradual modernization of logistics infrastructure. According to Makreo Research, Egypt now handles 1.5%–1.7% of global seaborne cargo, reinforcing its role as a strategic logistics gateway linking Europe, Asia, and Africa.

What is unfolding is not cyclical recovery, but a structural transformation. Infrastructure investment, policy-backed trade corridors, private-sector capital inflows, and sectoral demand from agriculture, manufacturing, retail, automotive, and e-commerce are reshaping Egypt’s logistics, warehousing, and cold chain ecosystem into an integrated, multi-modal platform with long-term growth visibility.

Makreo Research estimates Egypt’s freight market is projected to grow at a CAGR of 8.31% between 2025 and 2030, positioning the country among the fastest-expanding logistics markets across North Africa and the Eastern Mediterranean.

Freight Demand Structure Is Anchoring Market Expansion

Egypt’s freight demand remains concentrated across a core set of high-intensity sectors. In 2024, agriculture, manufacturing, construction, wholesale & retail trade, and oil & gas collectively accounted for approximately 85% of total freight transport demand, directly supporting sustained growth across logistics, warehousing, and third-party logistics (3PL) services.

Domestic freight movement remains overwhelmingly road-dominated, with nearly 80% of freight volumes transported via roadways. Trucks accounted for 96% of total freight movement as of 2023, underscoring the economy’s dependence on road logistics for time-sensitive and last-mile cargo flows. Rail and inland waterways together contribute less than 10%, though this balance is set to shift gradually as multimodal investments scale.

Agriculture and retail alone account for nearly 50% of domestic freight trips, moving more than 70 million tons of produce and consumer goods annually, with over 85% dependent on road transport. This concentration continues to fuel demand for dry warehousing, bonded storage, distribution centers, and temperature-controlled logistics. Manufacturing, contributing roughly 17% of Egypt’s GDP, generates steady inbound raw material flows and outbound finished goods movement, supporting value-added logistics services and large-format warehousing. Construction remains one of the most freight-intensive sectors, driven by large-scale government-led infrastructure projects and industrial zone development.

Maritime Connectivity Reinforces Egypt’s Role as a Global Trade Gateway

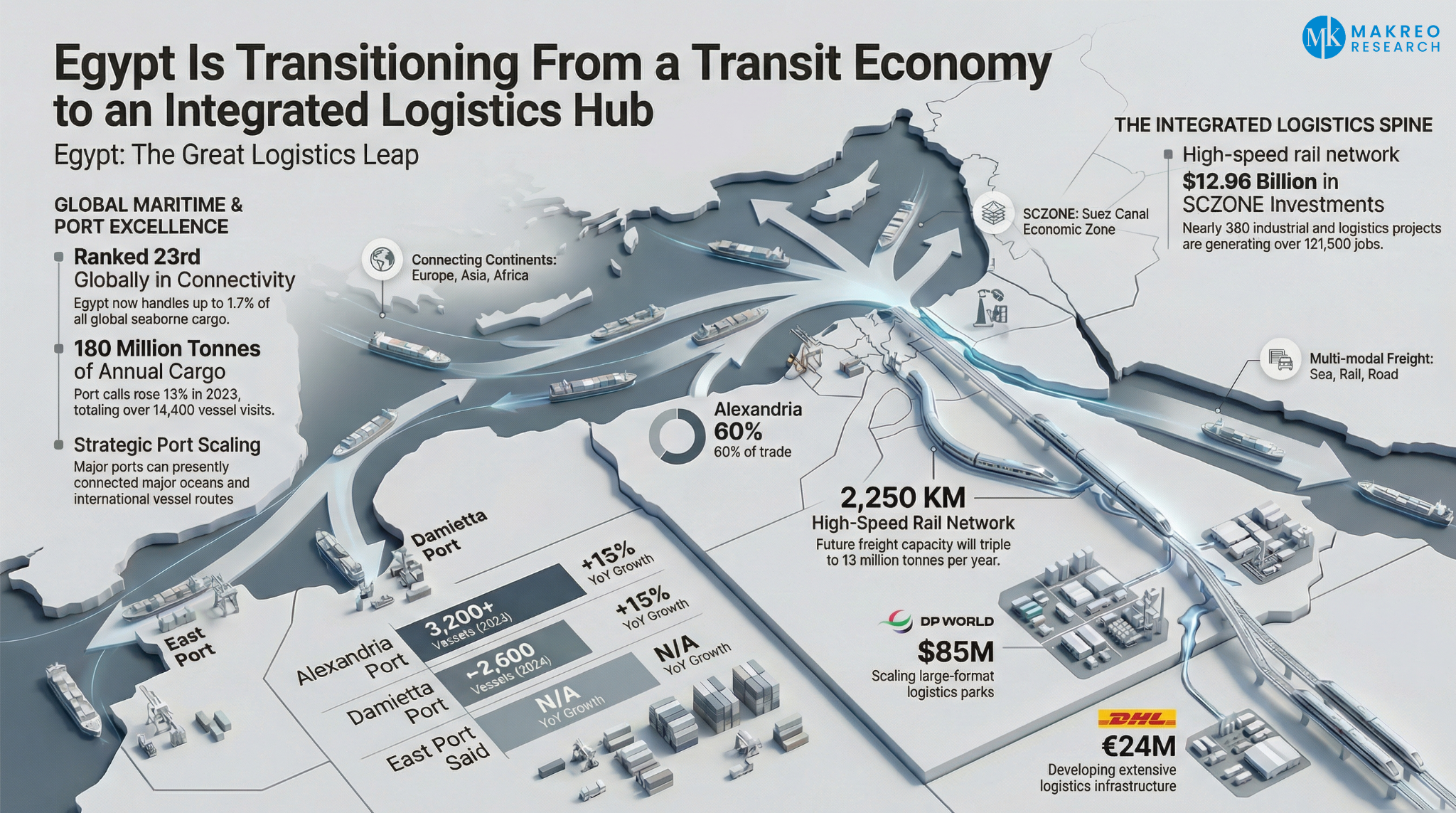

Egypt’s maritime competitiveness has strengthened materially over the past five years. In 2024, the country ranked 23rd globally on the Maritime Connectivity Index, reflecting sustained port modernization and its strategic geographic positioning.

In 2023, port calls increased by approximately 13% to over 14,400 vessels, while cargo throughput reached nearly 180 million tons. Egypt operates around 55 seaports, including 18 commercial ports and 37 specialized ports, supported by a 3,000 km coastline spanning the Mediterranean and Red Sea.

Key ports continue to scale throughput:

-

Alexandria Port handled over 3,200 vessels in 2024, up 13% year-on-year

-

Damietta Port processed approximately 2,600 ships, growing 15% YoY

-

Ain Sokhna surpassed 1.1 million TEUs

-

East Port Said exceeded 3 million TEUs, reinforcing Egypt’s transshipment role

Alexandria remains the country’s dominant trade gateway, handling over 60% of Egypt’s international trade, supported by extensive warehousing and refrigerated storage infrastructure.

The Suez Canal Corridor Is Becoming Egypt’s Logistics Spine

Egypt is actively positioning the Suez Canal corridor as a multi-node logistics, industrial, and manufacturing platform rather than a standalone maritime passage.

Confirmed investment contracts within the Suez Canal Economic Zone (SCZONE) reached USD 12.96 billion, covering nearly 380 industrial, service, and logistics projects, with an estimated 121,500 jobs expected to be generated. Nodes such as Sokhna and Qantara West are emerging as anchor locations for canal-linked logistics and manufacturing.

Sokhna, in particular, has become a focal point for integrated supply chains, combining port infrastructure, industrial land, and logistics parks. Notable investments include:

-

DP World, which inaugurated Sokhna Logistics Park with an initial investment of USD 85 million, targeting ~300,000 m² of capacity by 2026

-

DHL Express, which committed €24 million to its largest service center in East Cairo Logistics Park

-

Scan Global Logistics, entering Egypt as part of its MENAT expansion, citing a logistics and warehousing market valued at EGP 110 billion (2023)

These investments reflect long-term confidence in Egypt’s logistics fundamentals rather than short-term opportunistic capital deployment.

Dry Ports, Multimodal Corridors, and Rail Are Redefining Connectivity

Egypt’s logistics strategy increasingly emphasizes multimodal integration. The government has outlined plans to establish 33 dry ports and logistics zones nationwide, designed to reduce congestion at seaports, strengthen inland connectivity, and integrate industrial areas with road and rail networks.

A key enabler of this transition is Egypt’s high-speed electric rail network, expected to transport up to 13 million tonnes of freight annually, compared with just 4–5 million tonnes currently carried by conventional rail. The network will initially span 2,000 km, expanding to 2,250 km, linking major ports, industrial zones, agricultural regions, and dry ports across the country.

The rail system is designed to connect production zones such as New Delta, West Minya, Toshka, and the Future of Egypt project directly with export ports, reducing reliance on road freight while improving cost efficiency and sustainability.

Warehousing Is Consolidating Around Large-Format Logistics Nodes

Egypt’s warehousing landscape is transitioning from fragmented, small-scale facilities toward large-format, professionally managed logistics parks. In 2025, large warehouses account for the dominant share of national warehousing stock, concentrated around:

-

6th of October City

-

10th of Ramadan City

-

Alexandria

The Greater Cairo Region alone hosts an estimated 85 million m² of warehousing area, supported by over 10 major logistics nodes.

E-commerce and Q-commerce players are expanding aggressively:

-

Jumia operates a 27,000 m² smart warehouse along the Cairo–Suez Road

-

talabat mart inaugurated the largest Q-commerce distribution center in MENA (22,405 m²) in 2025

These facilities integrate automation, real-time inventory visibility, and last-mile optimization, signaling a shift toward technology-enabled fulfillment infrastructure.

Cold Chain Logistics Is Gaining Strategic Importance

Egypt’s cold chain market is entering a new growth phase. Makreo Research estimates the segment will grow at a CAGR of 5.66% between 2025 and 2030, despite operating costs being approximately 25% higher than neighboring markets.

Demand is driven by:

-

Export-oriented food processing

-

Aquaculture expansion (Egypt is Africa’s largest producer of farmed fish, with aquaculture accounting for 75%+ of production)

-

Pharmaceutical distribution

-

Rising consumer demand for fresh and processed food

Arab countries absorbed 54% of Egypt’s outbound cold chain volumes in 2024, underscoring regional demand strength. Notably, frozen potato exports surged 923% in 2024, reflecting improvements in cold chain reliability and export compliance.

On the supply side:

-

DP World and Elsewedy Industrial Development invested USD 29 million in a 25,000-pallet cold storage facility at Al Oula Industrial City

-

Capital Agro launched a USD 25 million frozen food logistics hub in Belbeis with 30,000+ pallet capacity, AI-enabled inventory systems, and renewable energy integration

-

Noatum Ports signed an MoU with Al Dahra Agriculture - Egypt to expand warehousing, customs clearance, and digital supply chain capabilities

Automotive, Agriculture, and E-Commerce Are Reshaping Demand

Egypt’s automotive industry is expected to cross 95,000 vehicle units by end-2025, accelerating inbound spare parts logistics and outbound vehicle distribution. The entry of global OEMs, including Tata Motors in partnership with MM Group, is expanding medium- and heavy-duty truck availability for logistics operators.

Agricultural production is projected to rise from EGP 3.3 trillion in 2024/25 to EGP 5.7 trillion by 2028/29, significantly expanding freight, warehousing, and cold chain requirements.

Meanwhile, Egypt’s e-commerce market, valued at USD 9.5 billion in 2025, is expected to nearly double to USD 18.7 billion by 2030, driving sustained demand for fulfillment centers, express delivery, and temperature-controlled storage.

The Long-Term Outlook: From Capacity Expansion to Integrated Logistics Ecosystem

Egypt’s logistics, warehousing, and cold chain market is transitioning from capacity-led growth to integration-led expansion. Accelerated port modernization, dry port development, multimodal corridors, and rising private-sector participation are reinforcing Egypt’s role as a regional logistics gateway connecting Africa, the Middle East, and Europe.

According to Makreo Research, the next phase of market evolution will be shaped by:

-

Large-format warehousing and multimodal logistics parks

-

Rising cold chain penetration across agri-exports and food processing

-

E-commerce and Q-commerce fulfillment scale-up

-

Automotive and industrial logistics specialization

-

Policy-backed port and trade corridor expansion

As infrastructure investments mature and trade flows stabilize, Egypt’s logistics ecosystem is entering a multi-dimensional growth phase with sustained opportunity for logistics operators, infrastructure developers, investors, and multinational supply chain participants.

Makreo Research’s study, "Egypt Logistics, Warehousing and Cold Chain Market Size and Forecast (2021–2030)", provides a comprehensive assessment of market size, segmentation, competitive dynamics, infrastructure development, and long-term forecasts shaping this transformation.

The question is no longer whether Egypt’s logistics market will scale, but how quickly it can integrate, digitize, and specialize to capture its full gateway potential.

Email us at info@makreo.com to discuss your research needs and explore how we can become your research partner in progress.

Explore our Custom Research & Market Survey Capabilities

Egypt logistics market, Egypt warehousing market, Egypt cold chain logistics, integration-led logistics growth, multimodal logistics Egypt, Suez Canal logistics corridor, dry ports Egypt, rail freight Egypt, logistics parks Egypt, large-format warehousing Egypt, cold chain infrastructure Egypt, e-commerce logistics Egypt, freight market forecast Egypt, logistics investment Egypt