Philippines Freight and Logistics Market Approaches USD 20 Billion by 2030 as E-Commerce, Infrastructure, and Investment Activity Reshape Supply Chains

Philippines logistics market approaches USD 20B by 2030, driven by e-commerce, infrastructure investment, and multimodal integration, transforming supply chains and efficiency.

The Philippines freight and logistics market is entering a structurally important phase of evolution. What was historically constrained by geographic fragmentation, infrastructure bottlenecks, and cost inefficiencies is now transitioning toward a more connected, technology-enabled logistics ecosystem. Between 2021 and 2025, the market expanded at a CAGR of approximately 2.6%, supported by stable trade flows, rising domestic consumption, and a sharp acceleration in e-commerce-driven logistics demand.

This is not a high-growth surge, but a measured, capability-driven transformation. Investments in port modernization, airport capacity expansion, inter-island connectivity, and digital freight platforms are gradually improving operational reliability, positioning the Philippines as an emerging logistics hub within Southeast Asia.

Makreo Research indicates that the Philippines freight and logistics market will continue to expand steadily through 2030, supported by infrastructure upgrades, growing outsourcing of logistics services, and increasing integration of multimodal transport systems.

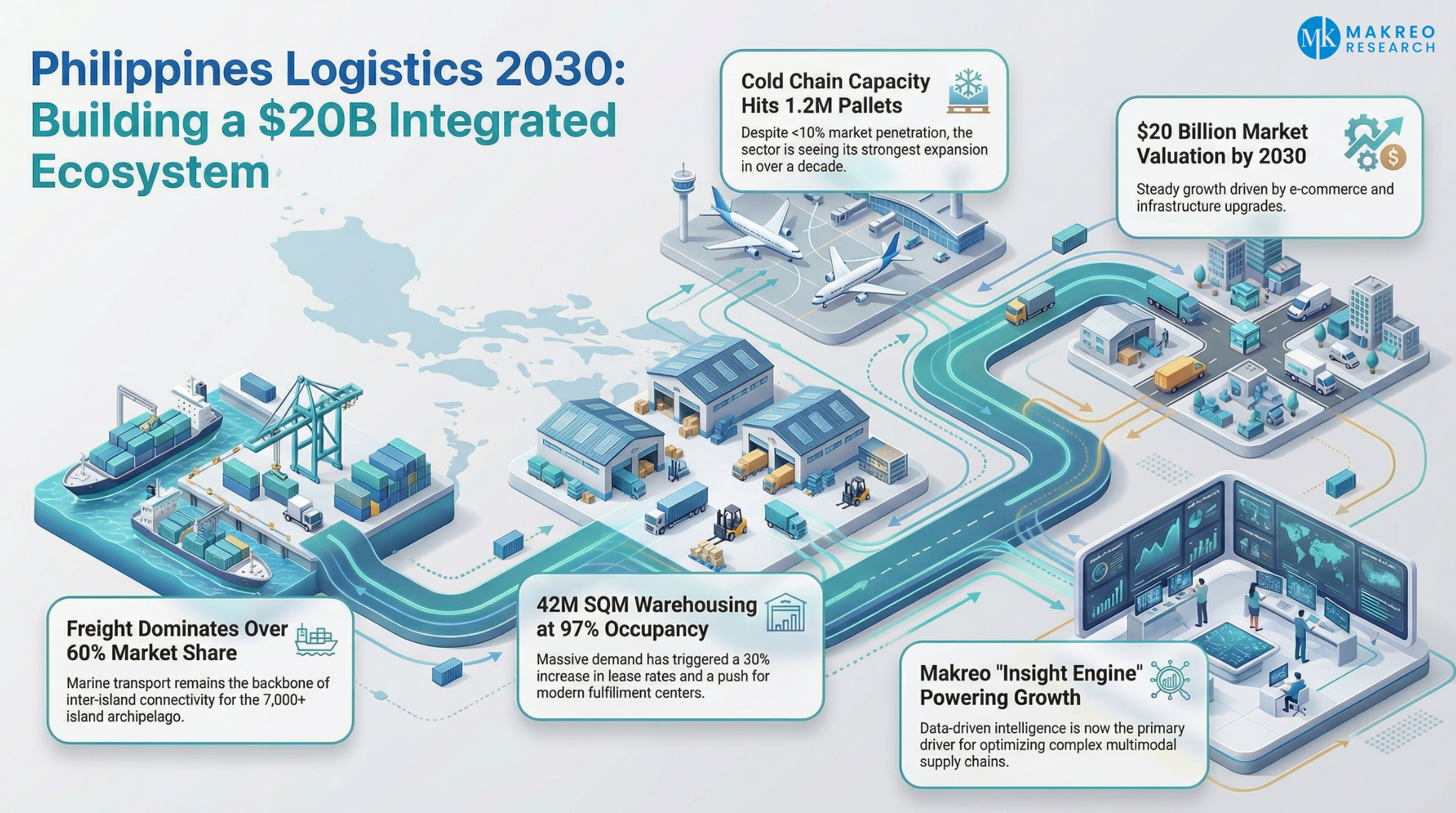

Freight Drives Over 60% of Logistics Activity in the Philippines

The Philippines logistics ecosystem remains heavily freight-centric, driven by the country’s geographic composition of more than 7,000 islands. Inter-island cargo movement continues to anchor logistics demand, with marine transport forming the backbone of long-haul freight, while road logistics dominates first-mile and last-mile connectivity, particularly across Luzon.

Freight demand is primarily concentrated across:

-

Domestic consumption and retail distribution

-

Agriculture and food supply chains

-

Manufacturing and industrial goods movement

-

Import-export trade flows

Despite the growing importance of warehousing and value-added logistics, freight continues to account for the majority share of logistics activity, reflecting the economy’s reliance on physical goods movement rather than service-led logistics.

At the same time, air freight is gaining relevance in high-value and time-sensitive segments, particularly driven by e-commerce, electronics, and pharmaceutical shipments.

Philippines Logistics Sees Strong Infrastructure Investment Push

Infrastructure development remains the most critical enabler of logistics efficiency in the Philippines. The government, along with private sector participants, is actively investing in improving cargo movement across ports, airports, and inland transport networks.

Key Infrastructure and Policy Developments:

-

Mindanao Railway Project (MRP)

Valued at approximately PHP 83 billion (~USD 1.5 billion), this 1,000+ km rail network aims to reduce travel time from 4 hours to 1 hour while enabling efficient freight movement for agriculture and mining sectors. -

Subic–Clark–Manila–Batangas (SCMB) Freight Railway

Supported by USD 4 million in U.S. technical assistance, this corridor is expected to significantly enhance freight connectivity across Luzon’s key industrial and port zones. -

Bauan International Container Terminal (Batangas)

ICTSI announced an USD 800 million investment to develop a terminal with 2 million TEUs annual capacity, with the first berth targeted by 2027. -

Marine Cargo Tariff Revision (2024)

A phased 16% tariff increase (10% + 6%) reflects ongoing efforts to fund infrastructure upgrades and improve port operations.

These developments indicate a clear policy direction toward multimodal integration, which remains underdeveloped but essential for reducing logistics costs and improving national supply chain efficiency.

Warehousing Expansion Intensifies Competition in Philippines

The Philippines warehousing segment is gaining momentum as logistics demand becomes more structured and time-sensitive. High occupancy levels, rising lease rates, and continuous supply expansion reflect a tightening market, while global players are accelerating the shift toward modern, technology-enabled warehousing.

Key Company-Led Developments:

-

Rhenus Group

Investing ~USD 20 million to expand operations, including a 20,000 sqm warehouse (by 2026) and scaling to 7 facilities nationwide, strengthening domestic coverage. -

DB Schenker

Strengthening integrated warehousing and distribution networks in a market operating at ~97% occupancy, reflecting tight capacity and rising need for end-to-end solutions. -

Maersk

Scaling its logistics and warehousing footprint in line with steady 4–5% annual supply expansion and growing multimodal integration requirements. -

SM Prime Holdings

Supporting modern warehouse supply through industrial park developments in hubs like Laguna, contributing to ~63% growth in industrial warehouse stock (2015–2025).

Key Market Indicators:

-

~42 million sqm warehouse supply (2025) with ~97% occupancy

-

4–5% annual supply growth expected through 2027

-

~30% increase in lease rates vs. pre-pandemic levels

-

~63% growth in industrial stock (2015–2025)

-

Cold chain capacity reached ~1.2 million pallet positions

The sector is evolving toward organized, high-spec, and integrated warehousing, with competition increasingly driven by quality, scale, and technology.

Key Logistics Players Expand Multimodal Networks in the Philippines

The Philippines freight and logistics market is becoming increasingly competitive, with both domestic and global players strengthening their operational footprint through multimodal integration and service expansion. Freight continues to dominate the ecosystem, contributing over 60% of total logistics activity, driven by inter-island cargo flows and growing domestic distribution demand.

Key Developments Across Leading Players:

-

2GO Group is strengthening its nationwide footprint by integrating marine and road logistics, positioning itself as a key enabler of inter-island cargo movement.

-

Maersk Filipinas is evolving from a conventional shipping provider into an end-to-end logistics partner, expanding its presence across inland transport and supply chain solutions.

-

DSV Logistics Solutions Philippines continues to scale its multimodal offerings, particularly in freight forwarding and contract logistics, to support more complex distribution requirements.

-

Schenker Philippines is enhancing its integrated logistics network, combining air, sea, and road capabilities with warehousing infrastructure to improve service efficiency.

-

FedEx has expanded its operations at Clark International Airport in 2024, significantly improving air freight capacity and strengthening express logistics connectivity for time-sensitive shipments.

-

A strategic partnership between 2GO Group and EVAP (2025) reflects early movement toward sustainable logistics, with a focus on fleet modernization and operational efficiency.

At the same time, the rapid growth of e-commerce is accelerating demand for courier, express, and parcel (CEP) services, pushing logistics providers to evolve from standalone freight operators to integrated, end-to-end supply chain partners.(point)

As competition intensifies, differentiation is increasingly defined by network reach, multimodal capability, and service integration, rather than scale alone.

Philippines Cold Chain Market is Gaining Momentum

Cold chain logistics in the Philippines accounts for <10% of the market, but is becoming increasingly important with rising demand from food, pharmaceuticals, and export sectors.

Despite its small base, growth is accelerating:

-

Capacity reached ~1.2 million pallet positions (2025), the strongest growth in over a decade

-

Supply has increased 35%+ vs. pre-pandemic levels

-

Expansion is extending beyond Metro Manila into Visayas and Mindanao

Growth is driven by higher demand for perishables, pharma distribution, and export logistics.

However, challenges remain:

-

High capex and energy-intensive operations

-

Limited last-mile cold chain infrastructure

-

Logistics costs reaching ~25–27% of product value

The sector is still in a catch-up phase, making cold chain a key investment priority for improving efficiency and reducing supply chain losses.

Philippines Logistics Shifts to Integrated Multimodal Ecosystem

The Philippines freight and logistics market is gradually transitioning from a fragmented, capacity-constrained system toward a more integrated and technology-enabled logistics ecosystem. Continued investments in port modernization, airport expansion, inter-island connectivity, and warehousing infrastructure are strengthening the country’s logistics backbone and improving overall supply chain efficiency.

As these developments scale, the market is expected to move beyond basic freight movement toward more coordinated, multimodal logistics networks that support faster, more reliable, and cost-efficient cargo flows across regions.

According to Makreo Research, the next phase of market evolution will be shaped by:

-

Expansion of multimodal transport networks across marine, road, air, and rail

-

Strengthening of inter-island logistics and regional connectivity beyond Luzon

-

Rapid growth of e-commerce and CEP-driven logistics infrastructure

-

Scaling of organized warehousing and fulfillment centers

-

Gradual development of cold chain logistics for food and pharmaceutical sectors

-

Increased adoption of digital freight platforms and real-time supply chain visibility

As infrastructure investments mature and logistics networks become more integrated, the Philippines is expected to strengthen its position as a high-potential logistics and trade hub within Southeast Asia, supported by rising domestic demand and improving connectivity.

Makreo Research’s study, "Philippines Freight and Logistics Market Size and Forecast (2021–2030)", provides a comprehensive assessment of market size, segmentation, competitive landscape, infrastructure development, and long-term forecasts shaping this transformation.

The question is no longer whether the Philippines logistics market will expand, but how effectively it can integrate, modernize, and scale its logistics capabilities to unlock its full potential as a connected island economy.

Email us at info@makreo.com to discuss your research needs and explore how we can become your research partner in progress.

Explore our Custom Research & Market Survey Capabilities.

Philippines logistics market, Philippines freight market, Philippines market research, Philippines market survey, custom research Philippines, Southeast Asia logistics, Philippines supply chain, logistics market growth Philippines, Philippines e-commerce logistics, warehousing Philippines, cold chain Philippines, multimodal logistics Philippines, Philippines infrastructure logistics, freight transport Philippines, inter-island logistics Philippines, CEP market Philippines, logistics companies Philippines, logistics investment Philippines, Philippines trade logistics, emerging logistics markets Asia