India's Oral Care Market The Premiumisation Shift, D2C Growth, and the Consumer Gaps Most Brands Are Missing -

India’s oral care market is evolving into a USD 5B ecosystem, driven by premiumization, D2C growth, and shifting consumer behavior, yet key gaps in adoption and awareness remain.

India's Oral Care Market Is Undergoing a Category-Level Structural Shift

Walk into any kirana store in India today and watch what happens at the oral care shelf. A decade ago, the shopper picked up a tube of toothpaste and moved on. Today, she is reading the back of a whitening serum, comparing mouthwash variants, and mentally noting an electric toothbrush brand she discovered on Instagram last night. She is behaving like a beauty shopper, not a hygiene buyer on autopilot. That shift in behaviour is the real story of India's oral care market, and it is happening faster than most brands have prepared for.

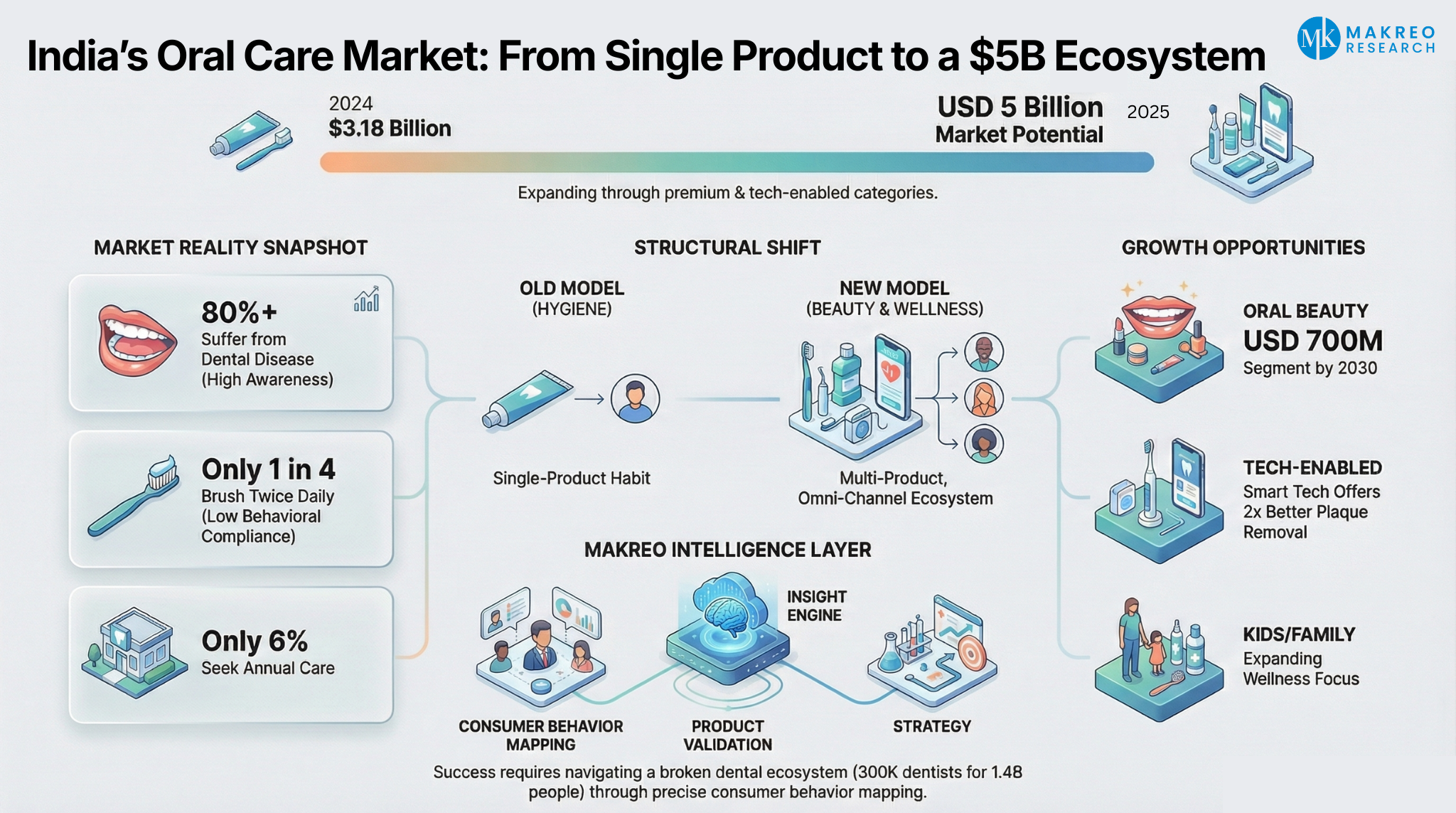

The numbers confirm the structural change. India's oral care market, valued at USD 3.18 billion in 2024, is projected to approach USD 5 billion by 2030, but the more significant story is in the composition of that growth. Toothpaste still anchors the category at ~70% of sales, yet the incremental demand is flowing into mouthwashes, whitening formats, sensitivity solutions, and tech-enabled devices. Only 1 in 4 Indians brushes twice daily. Over 80% suffer from some form of dental disease. And 32 funded D2C oral care brands are now competing for the urban consumer's attention. This is no longer a one-product market, it is a category in the middle of a structural reset.

This is where Makreo Research's custom research and market survey capabilities become critical, not simply mapping what the market looks like, but decoding why consumers behave as they do, where demand is genuinely forming, and which decisions, product, pricing, channel, or geography, are being made on assumptions rather than evidence.

What the Market Looked Like Before, and What Is Changing Now

To understand where India's oral care market is going, it helps to be clear about where it came from. For the better part of three decades, the category was defined by a few structural constants:

• Product concentration: Toothpaste was the category. Toothbrushes were functional afterthoughts, replaced infrequently. Mouthwash was niche, largely hospital-adjacent. Floss was aspirational, something that belonged in hotel bathrooms, not household routines.

• Brand concentration: Colgate alone held ~43% market share, with Pepsodent (~23%) and Dabur (~17%) rounding out a top-heavy competitive structure. The top three players collectively controlled 80–85% of the market.

• Purchase behavior: Buying was habitual and price-anchored. Switching costs were low, but switching rates were even lower. India's per capita oral care spend remained significantly below global peers.

• Channel concentration: The trade was dominated by general trade, kiranas, medical stores, and local chemists. Modern retail was an urban phenomenon. Digital commerce did not exist as a meaningful oral care channel.

Each of these structural constants is now under pressure, some shifting gradually, others changing with surprising speed.

The most consequential shift is not product proliferation but consumer intention. A growing segment of Indian consumers, led by urban millennials and Gen Z is beginning to approach oral care the way they approach skincare: with awareness of ingredients, concern for specific conditions, and a preference for brands that speak their language. This is a fundamentally different demand signal than the one FMCG companies have historically responded to.

How Makreo Research Delivers Strategic Clarity in India's Oral Care Market

Case Study: Unlocking Premium Oral Care Growth in Tier 2 India

The Business Challenge

A leading herbal oral care brand with strong metro distribution faced a persistent gap: high brand awareness in Tier 2 and Tier 3 cities, but disproportionately low conversion to premium SKUs. Secondary data confirmed that India's premium oral care market was growing nationally, yet the brand's premium revenue remained overwhelmingly metro-concentrated. The question was not whether the opportunity existed, but why consumer behaviour in Tier 2 cities was not reflecting it, and what would change that.

Makreo's Research Design

Makreo deployed a multi-methodology primary research program: a quantitative survey (n=1,800) across 12 cities mapping purchase triggers, price thresholds, and channel preferences by city tier, qualitative depth interviews (n=48) exploring ingredient trust, dentist influence, and conversion barriers in semi-urban households, a retail channel audit across 30 stores in 6 cities assessing SKU visibility and shelf dynamics in modern trade, pharmacy, and general trade, and expert consultations with 12 dental professionals to decode professional recommendation behaviour and patient awareness patterns.

Key Findings

• Price anchoring, not brand distrust. Tier 2 consumers did not distrust the brand, they associated premium oral care pricing with metro consumption contexts. The barrier was perceptual, not product-led.

• Dentist recommendation was decisive in Tier 2, far more than in metros. For sensitivity and medicated formats, 67% of Tier 2 consumers rated a dentist recommendation as 'very important' or 'essential' to trying a new product, compared to 42% in metro markets, directly undermining the brand's marketing-led entry strategy for medicated SKUs.

• E-commerce outperformed in-store for mouthwash and whitening. For these formats, e-commerce showed 2.3x higher conversion intent in Tier 2 cities than physical retail, driven by availability of trial-size SKUs absent from local general trade.

• The real unmet need was family-format products. The highest-demand opportunity in Tier 2 was not whitening or sensitivity, it was multi-benefit toothpastes that could serve an entire household without requiring multiple SKU decisions. Metro-derived segmentation assumptions had obscured this entirely.

Each of these structural constants is now under pressure, some shifting gradually, others changing with surprising speed.

The most consequential shift is not product proliferation but consumer intention. A growing segment of Indian consumers, led by urban millennials and Gen Z, is beginning to approach oral care the way they approach skincare: with awareness of ingredients, concern for specific conditions, and a preference for brands that speak their language. This is a fundamentally different demand signal than the one FMCG companies have historically responded to.

Strategic Outcomes

Makreo's insights reshaped the brand's Tier 2 go-to-market strategy across three clear pivots: premium SKUs were repositioned around 'value for your family' messaging rather than individual efficacy claims, a dedicated dental professional outreach program was built for medicated formats in Tier 2 clinic channels, and digital spend was redirected toward e-commerce trial-size formats for mouthwash and whitening, shifting investment from brand awareness to category trial.

Within two quarters, the brand's premium conversion in Tier 2 cities improved materially, not because the market had changed, but because the strategy had finally been aligned with consumer reality rather than category assumptions.

The Real Challenges and Gaps: Where the Market Is Actually Stuck

India's oral care market is frequently discussed in terms of its growth potential. The less examined, and more strategically important, story is about the structural gaps and behavioural failures that constrain that potential. For brands, investors, and D2C players, these are not background headwinds. They are the primary decision risks.

-

Awareness and Behaviour Are Not the Same Thing

Despite decades of advertising, only 1 in 4 Indians brush twice daily, over 80% suffer from dental disease, and just 6% seek annual treatment. These are not knowledge gaps but deep attitudinal and structural barriers. For brands, the key question is not awareness of fluoride, but trust in it, and whether premium pricing signals efficacy or overpricing. Only primary research captures this reliably. -

Rural India Is Not One Market, It Is Many

Rural India is a major growth opportunity, with over 95% of adults affected by dental caries and traditional practices like neem, coal, and salt still prevalent. However, treating it as one market is flawed. A semi-urban Tamil Nadu district differs significantly from rural Uttar Pradesh or Odisha. Single SKU, pan-India strategies have underperformed. What is needed is district-level primary research, not broad secondary data. -

Digital Discoverability Is Not the Same as Conversion

India’s e-commerce market exceeds USD 90 billion, with oral care growing rapidly across Amazon, Flipkart, and Nykaa. Colgate alone spends ₹800+ crore on advertising, increasingly digital. Yet impressions do not equal conversion or loyalty. Consumers often discover online but purchase offline. Mapping this non-linear journey across category, geography, and consumer profile is essential and cannot be solved through desk research. -

The Dental Ecosystem Is Structurally Broken, and That Limits Product Adoption

India has ~300,000 dentists for 1.4 billion people, with 95–97% clinics unorganised and lacking standardisation. This limits clinical endorsements and structured recommendation channels. Players like Clove Dental, with 650+ clinics, ₹378 crore FY2025 revenue, and USD 133 million funding, are improving access but still cover a small share. Weak dental infrastructure remains a core constraint to scaling premium and medicated products. -

D2C Oral Care Brands Are Caught in a Profitability Trap

India has 32 D2C oral care brands across segments. Perfora reached INR 70 crore revenue in four years with USD 8.4 million funding. However, high CAC, discounting, and heavy digital spend are compressing margins. The root issue is weak consumer insight. Many brands rely on assumptions from social listening rather than validated demand research, leading to inefficient product and pricing strategies.

Industry Signal: Capital Is Moving, Intelligence Must Keep Pace

October 2025 - Dabur Ventures: Dabur India launched a dedicated INR 500 crore investment platform to back high-growth D2C businesses across personal care, healthcare, wellness, and ayurveda, signalling that legacy FMCG players are now actively acquiring the digital consumer segments they cannot grow organically.

February 2025 - Colgate Total Active Prevention System: Colgate-Palmolive launched a three-product system — reformulated toothpaste, toothbrush, and mouthwash, designed to work together as an integrated oral care regime. A direct response to multi-product adoption trends.

July 2025 - Oracura Smart Toothbrush: Navi Mumbai-based oral care innovator Oracura unveiled a smart toothbrush with seamless app integration, offering real-time brushing insights and data-driven feedback, reflecting the growing viability of tech-enabled oral care even in the Indian market.

September 2025 - Clove Oral Care Product Line: Clove Dental's consumer-facing brand launched a new range of dentist-developed products, clean-ingredient toothpaste and ultra-soft ergonomic toothbrushes, directly leveraging its clinical network to build consumer brand trust.

Where the Genuine Opportunities Lie in India's Oral Care Market

The headline growth story for India's oral care market is real. But growth is not uniformly distributed, and the brands and investors that will capture disproportionate value are those that understand where, among whom, through which channels, and with what positioning the next phase of category expansion will occur.

Oral Beauty - A USD 700 Million Premium Segment in Formation

The emergence of oral care as a beauty and grooming category, not merely a hygiene category, is the most structurally significant demand shift occurring in India's oral care market today. Honasa Consumer estimates that the oral beauty segment could evolve into a USD 700 million opportunity by 2030, driven by teeth whitening products, cosmetic formulations, and premium oral care solutions targeting appearance and confidence.

This shift has a direct parallel in the evolution of skincare from functional ('moisturiser') to aspirational ('ceramide barrier repair serum'). The consumer is the same; the framing and the pricing architecture is different. Brands that can successfully reposition oral care within a beauty narrative on packaging, on digital channels, and in influencer ecosystems can access a higher-margin demand tier that the legacy FMCG channel does not currently serve.

The research question this opens is not 'is there demand for oral beauty products?' but 'which consumer segments have the aesthetic motivation, price tolerance, and channel preference to convert?' That distinction requires primary survey work not secondary data.

Technology-Enabled Oral Care - High Potential, Structurally Early

Electric toothbrush penetration in India remains in the single digits despite the category delivering up to 2x more plaque removal compared to manual brushes. Smart toothbrushes featuring AI-driven tracking, pressure sensors, and real-time feedback represented in India by players such as Oracura and Perfora are gaining traction among urban millennials but have not yet achieved the awareness or accessibility needed for mainstream adoption.

This gap represents a classic market development opportunity that requires awareness investment, distribution building, and price-point calibration across income segments. The research imperative here is to understand what triggers and sustains adoption among early adopters, and what barriers price, perceived complexity, or lack of dental professional endorsement prevent conversion among the next tier.

The Kids and Family Segment - Lifelong Value at Low Acquisition Cost

Children's oral care is an underdeveloped but strategically important segment in India. Dabur's December 2024 entry into the kids' toothpaste market with character-licensed variants designed for children over 3 years signals recognition of the category's strategic value: brands that establish oral care habits in childhood create consumers who are, structurally, lifelong buyers.

The research complexity in this segment is that the buyer and the user are different people. Parents are the purchasing decision-makers, and their motivations, safety of ingredients, dentist recommendation, child acceptability do not always align with the signals that FMCG marketing typically optimises for. Understanding the parent's mental model for their child's oral health is a primary research challenge, not a secondary data question.

How Makreo Research Supports India's Oral Care Market

As India's oral care market becomes more complex, more competitive, and more insight-dependent, the difference between brands that grow and brands that stall is increasingly a research quality problem. Not a product quality problem. Not a distribution problem. A decision quality problem = rooted in insufficient, or incorrectly structured, consumer intelligence.

Makreo Research supports FMCG brands, healthcare providers, investors, and emerging D2C players in navigating India's oral care market through the following research capabilities:

Consumer Behaviour Mapping

-

What triggers oral care product trial, switching, and loyalty in different consumer segments?

-

How do attitudinal barriers to dental care translate into product adoption rates?

-

What is the price elasticity of premium oral care formats across metro and non-metro markets?

Product Launch Readiness and Concept Validation

-

Formulation and ingredient trust assessment before launch

-

Pack size and pricing architecture validation across income segments

-

Innovation white-space identification in whitening, sensitivity, and herbal formats

Retail and Channel Strategy

-

Store-level audit of oral care shelf dynamics in general trade, modern trade, and pharmacy

-

E-commerce channel performance analysis across Amazon, Nykaa, Flipkart, and D2C platforms

-

Tier 2 and Tier 3 distribution readiness assessment

Competitive Intelligence and Benchmarking

-

Brand positioning and consumer perception mapping across incumbent and challenger brands

-

Herbal vs. clinical vs. experiential positioning effectiveness analysis

-

D2C brand performance benchmarking and switching behaviour research

Market Entry and Expansion Strategy

-

City-tier and demographic sizing for priority product categories

-

Go-to-market strategy development grounded in primary demand research

-

Investor-ready market assessments for new category entrants

Contact us at info@makreo.com to discuss your research needs and explore how Makreo can become your strategic intelligence partner in India's oral care market.

Market Research, Custom Research, India oral care market, oral care market India, India dental care industry, oral care market trends India, India toothpaste market size, India oral care industry analysis, India dental health statistics, premium oral care India, oral care premiumisation India, D2C oral care brands India, oral care consumer behavior India, oral care market growth India, oral care industry report India, India oral care market forecast 2030, dental issues in India statistics, oral hygiene habits India, why Indians don’t brush twice daily, oral care awareness vs behavior India, dental care gap India, oral care adoption challenges India, oral care market research India, custom market research India FMCG, oral care D2C strategy India, e-commerce oral care India, FMCG oral care insights India