India Mental Health & Wellness Market Where 200 Million People Need Care, But 80% Never Receive it

India’s mental health market is rapidly expanding, driven by rising demand, digital access, and D2C wellness trends, yet 80% remain untreated, creating a massive growth opportunity.

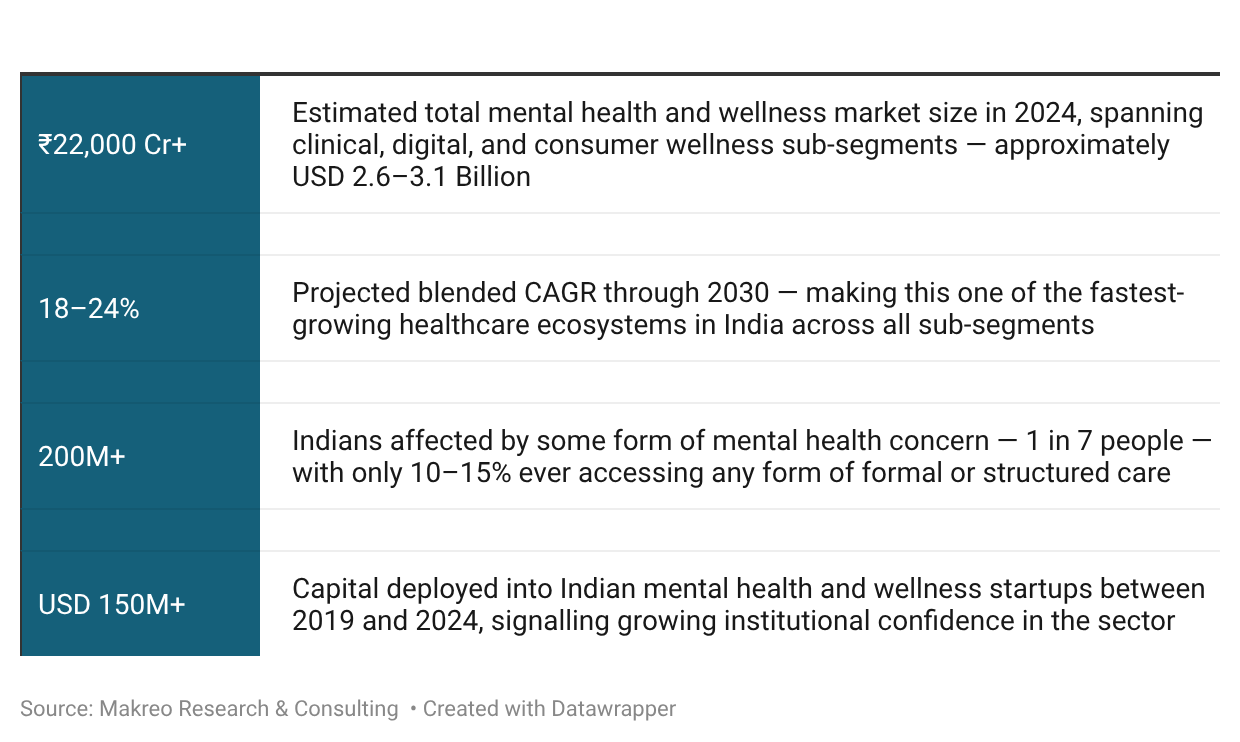

India's mental health and wellness market, spanning clinical care, digital platforms, D2C wellness products, nutraceuticals, functional foods, and corporate wellness programmes, is at a clear inflection point. After years of fragmentation and stigma-driven suppression, the market is beginning to reorganise around new delivery models, rising consumer awareness, and structural demand that has gone unaddressed for decades.

These numbers, significant as they are, still understate the true opportunity. They do not fully capture the informal care economy, the shadow wellness consumption market, or the massive suppressed demand in Tier 2, Tier 3, and rural India populations that are aware of their mental health needs but have no organised channel through which to address them.

Why This Market Is Growing Differently

Most healthcare markets grow in proportion to population demographics or income levels. India's mental health and wellness market does not follow that pattern. It is growing because of a simultaneous convergence of structural forces that are accelerating each other — creating a compounding demand dynamic that is unlike any other segment in India's healthcare economy.

The Demand Is Structural, Not Cyclical

The most critical insight for any organisation evaluating this market is that its demand is not reactive or episodic, it is structurally embedded into India's economic and social fabric.

-

1 in 7 Indians (14%+) experience a mental health disorder. This is not a post-pandemic spike, it is a baseline reality that has been building for two decades

-

Indian young adults aged 18–34 rank 60th out of 84 countries in the global Mind Health Quotient (MHQ) study, scoring just 33 out of 100 — the most digitally and economically active cohort in the country is also its most mentally fragile

-

Long working hours, always-on digital culture, job insecurity, and rising performance pressure have made workplace stress structural rather than situational, embedded into the daily operating reality of millions of Indian professionals

-

Post-pandemic residual anxiety and burnout have not resolved. Research consistently shows that the mental health burden from the pandemic continues to compound across income groups, age segments, and geographies

Two Markets Are Growing Simultaneously

What makes India's mental health landscape unusual is that it is not one market — it is two distinct but increasingly interconnected markets growing in parallel:

Clinical Mental Health

- Focuses on diagnosis, therapy, psychiatric care, and digital therapy platforms

- Driven by treatment needs (reactive, condition-based)

- Consumer entry via psychiatrists, therapists, or digital therapy apps

Consumer Mental Wellness

-

Includes supplements, functional foods, wellness apps, D2C products, and corporate wellness

-

Driven by prevention and performance (proactive, lifestyle-based)

-

Consumer entry via social media, D2C brands, or corporate wellness programmes

These two markets are converging at the edges, with digital therapy platforms adding wellness features, and wellness brands adding clinical credibility through research and professional endorsements. Understanding where a consumer sits on this spectrum, and how they move between the two, is one of the most important research questions in the market today.

Supply-Side Analysis: Infrastructure That Is Not Keeping Pace

If demand is the engine of India's mental health market, the supply side is the constraint, a deeply underdeveloped infrastructure that creates the defining tension in this sector. The gap between what is needed and what exists is not narrowing. It is widening. And it is this widening gap that creates the structural case for private investment, digital innovation, and consumer wellness solutions.

Public Infrastructure: Limited Scale, Uneven Distribution

India's public mental healthcare infrastructure, despite meaningful policy effort over the past decade, remains critically inadequate relative to the scale of need. The numbers reflect progress in isolation - but context reveals the depth of the shortfall.

.png) The spatial distribution of this limited infrastructure compounds the problem further. The vast majority of mental health professionals and facilities are concentrated in the top 8 metropolitan areas, leaving Tier 2, Tier 3, and rural India almost entirely dependent on the severely under-resourced public system or on no care at all.

The spatial distribution of this limited infrastructure compounds the problem further. The vast majority of mental health professionals and facilities are concentrated in the top 8 metropolitan areas, leaving Tier 2, Tier 3, and rural India almost entirely dependent on the severely under-resourced public system or on no care at all.

Digital Infrastructure: The Emerging Access Layer

While physical infrastructure remains critically constrained, digital initiatives, both government-led and private sector are creating an alternative access layer that is beginning to reshape how mental health services reach India's population. This digital layer is not a replacement for clinical care. It is a new category of access that sits between the unmet need and the clinical system catching the vast majority who would otherwise receive nothing.

Tele-MANAS (14416)

- Type: Government

- Offers 24x7 helpline and mobile app for nationwide mental health support

- Reach: National (app launched in 2024)

- Significance: First nationwide free digital mental health touchpoint

NTMHP

- Type: Government

- Enables remote clinical services under the National Tele-Mental Health Programme

- Reach: Active since 2022

- Significance: Facilitates psychiatrist consultations via telehealth

iCall

- Type: NGO / Digital

- Provides TISS-backed counselling helpline and digital therapy for students and professionals

- Reach: Urban-focused

- Significance: Strong credibility among youth and academic segments

Vandrevala Foundation

-

Type: NGO / Digital

-

Offers 24x7 mental health helpline with multi-language support

-

Reach: Nationwide, available in 16 languages

-

Significance: One of India’s widest-reaching free support services

Wysa

- Type: Private / AI

- AI-powered emotional wellness app with therapist escalation options

- Reach: Global with strong India presence

- Significance: Leader in AI-assisted mental wellness at scale

YourDOST

- Type: Private / B2B

- Online therapy platform with strong corporate and campus presence

- Reach: B2B enterprise + B2C

- Significance: Pioneer in corporate mental wellness in India

The Wellness Market: Where Mental Health Meets D2C Healthcare Products

The Indian mental wellness and D2C healthcare products market, encompassing nutraceuticals, adaptogens, functional foods and beverages, sleep products, wellness apps, and personal care products with mental wellness claims, represents a significant and fast-moving segment within the broader mental health economy.

₹9,000 Cr+ is the current size of India’s mental wellness and D2C healthcare products market in 2024. This includes supplements, functional foods, sleep products, and wellness apps, and the segment continues to grow rapidly.

The segment is projected to grow at a CAGR of 24 to 28 percent through 2030, outpacing the broader mental health market growth rate by 6 to 10 percentage points.

There has been a 3X growth in Indian nutraceuticals focused on cognitive and emotional wellness between 2020 and 2025, driven by a post-pandemic shift toward preventive health.

USD 400M+ has been invested across India’s D2C wellness sector, including nutrition, supplements, and mental wellness, between 2021 and 2024. Mental wellness-focused brands are now attracting Series A funding rounds ranging from USD 5 to 15 million.

This segment is being driven by a new generation of Indian consumers, primarily urban, digitally native, and aged between 22 and 38. These consumers are proactively investing in mental performance and emotional resilience as part of their daily health routine, rather than waiting for clinical intervention.

They are not patients, but wellness consumers, and they represent the fastest-growing buyer segment in India’s healthcare economy.

Product Categories Driving D2C Mental Wellness Growth

The Indian D2C mental wellness market spans a wide and rapidly expanding range of product categories. Understanding the relative growth stage, consumer motivation, and research priority of each is essential for any brand, investor, or strategist evaluating this space.

.png)

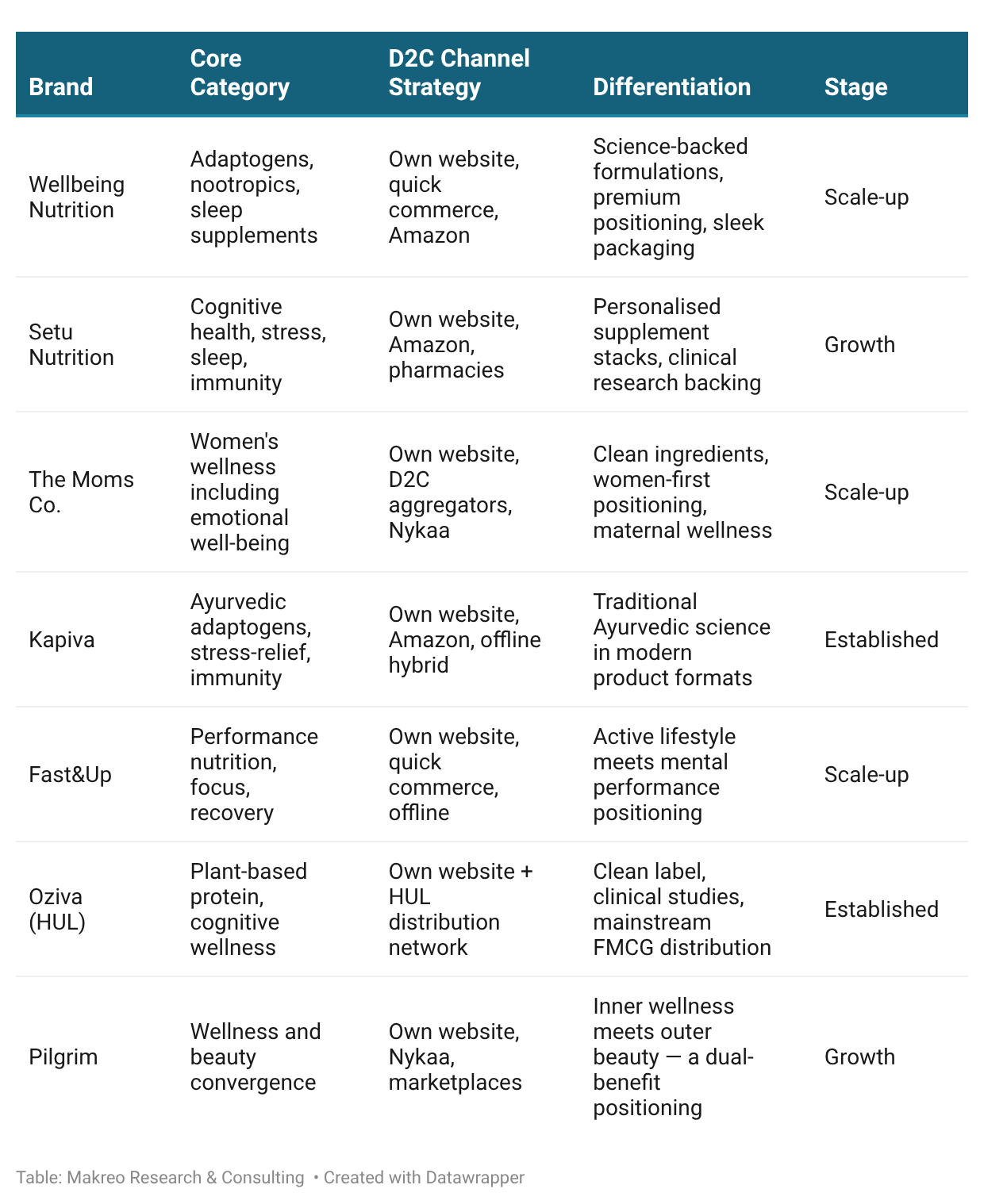

Key D2C Mental Wellness Brands Shaping India's Market

India's D2C mental wellness landscape is evolving rapidly, moving from early-stage experimental brands to a competitive ecosystem of scale-stage players attracting significant capital, building real consumer bases, and beginning to capture category leadership positions. The brands listed below represent the current leaders, challengers, and emerging disruptors shaping the competitive map.

Three Most Important Competitive Dynamics

1. The Credibility Race in D2C Wellness

As the D2C mental wellness market matures from early adopters to mainstream consumers, clinical credibility is rapidly becoming the defining competitive differentiator. Consumer scepticism about supplement efficacy is the single largest barrier to category expansion in India. Brands that invest in third-party clinical validation, transparent ingredient sourcing, and regulatory-compliant health claims will create a credibility moat that content marketing alone cannot replicate.

2. The Tier 2/3 Expansion Race

The next phase of growth for every segment digital therapy, D2C wellness, corporate wellness, and functional food will come from Tier 2 and Tier 3 cities. These are markets with rapidly rising awareness, genuine unmet need, and almost no organised private sector presence. The first players to build culturally contextual, regionally relevant, and price-appropriate solutions for these markets will capture category leadership before competitive intensity arrives.

3. The Channel Convergence Opportunity

The most underexplored competitive opportunity in India's mental health and wellness market is the integration of digital therapy with D2C wellness products a full-stack mental wellness platform that addresses both the clinical and the lifestyle dimensions of mental health in a single consumer relationship. No Indian brand has yet credibly built this integrated model, and the window for doing so is open.

How Makreo Research Supports Decision-Making in This Market

As India's mental health and wellness market becomes more complex, insight-driven, and competitively intense, the quality of research inputs directly determines the quality of strategic outcomes. At Makreo Research, we help organisations move from market awareness to market action through rigorous, primary-research-led intelligence designed specifically for high-growth, high-complexity sectors.

Consumer Behaviour Mapping

- Analyses awareness, stigma, help-seeking behavior, and willingness to pay across demographics

- For digital platforms, NGOs, D2C brands, policy organisations

Market Opportunity Assessment

- Sizes demand by segment, city tier, and demographics

- Identifies 3–5 year growth opportunities

- For investors, planners, new entrants

Product and Platform Validation

- Pre-launch testing for therapy solutions, wellness products, and clinical services

- For startups, product teams, D2C founders

D2C Wellness Brand Research

- Covers consumer profiling, claims validation, and purchase journey

- Builds channel strategies

- For D2C brands, FMCG players, VC-backed companies

Go-to-Market Strategy Research

- Defines pricing, channels, positioning, and expansion strategy

- Focus on metro and Tier 2/3 entry

- For growth-stage and international brands

Competitive Intelligence

- Tracks players, pricing, differentiation, and funding trends

- Identifies market gaps

- For strategy teams and investors

Corporate Wellness Research

- Evaluates HR decisions, EAP adoption, and employee demand

- Builds ROI frameworks

- For EAP providers and enterprise platforms

Entering or expanding in India’s mental wellness market

Build a strong research foundation to reduce risk

India mental health market, mental wellness India, D2C wellness India, mental health industry India, wellness market growth India, mental health startups India, digital mental health India, corporate wellness India, mental health statistics India, healthcare market India, nutraceuticals India market, functional foods India, mental wellness trends India, preventive healthcare India, AI mental health apps India, therapy platforms India, mental health investment India, wellness brands India, consumer wellness India, healthcare research India, market research India, mental health awareness India, wellness economy India, behavioral health India