Global Solar PV Market Reaches ~3 TW in 2025, Signaling a Structural Shift in Energy Systems

The global solar PV market reaches ~3 TW in 2025, driven by Asia Pacific, China, India, and solar-plus-storage adoption, signaling a structural shift in global energy systems.

The global solar photovoltaic (PV) market has crossed a threshold that few energy technologies have achieved within such a compressed timeframe. By 2025, cumulative installed solar PV capacity is approaching ~3 terawatts, positioning solar as one of the largest sources of new power capacity ever deployed globally. This milestone reflects not just scale, but a fundamental transformation in how solar PV is integrated into power systems, supply chains, and long-term energy planning.

The previous five years were defined by rapid capacity additions, aggressive cost compression, and unprecedented manufacturing scale, largely centered in Asia. The next phase of growth, however, is being shaped by a different set of forces: policy volatility, grid integration constraints, supply-chain diversification, and the accelerating convergence of solar with energy storage.

This transition is already visible across Asia Pacific, China, India, Europe, North America, and select emerging markets, where solar PV is shifting from a marginal renewable option into foundational energy infrastructure.

Asia Pacific Anchors Global Solar PV Market Growth, but Regional Momentum Is Fragmenting

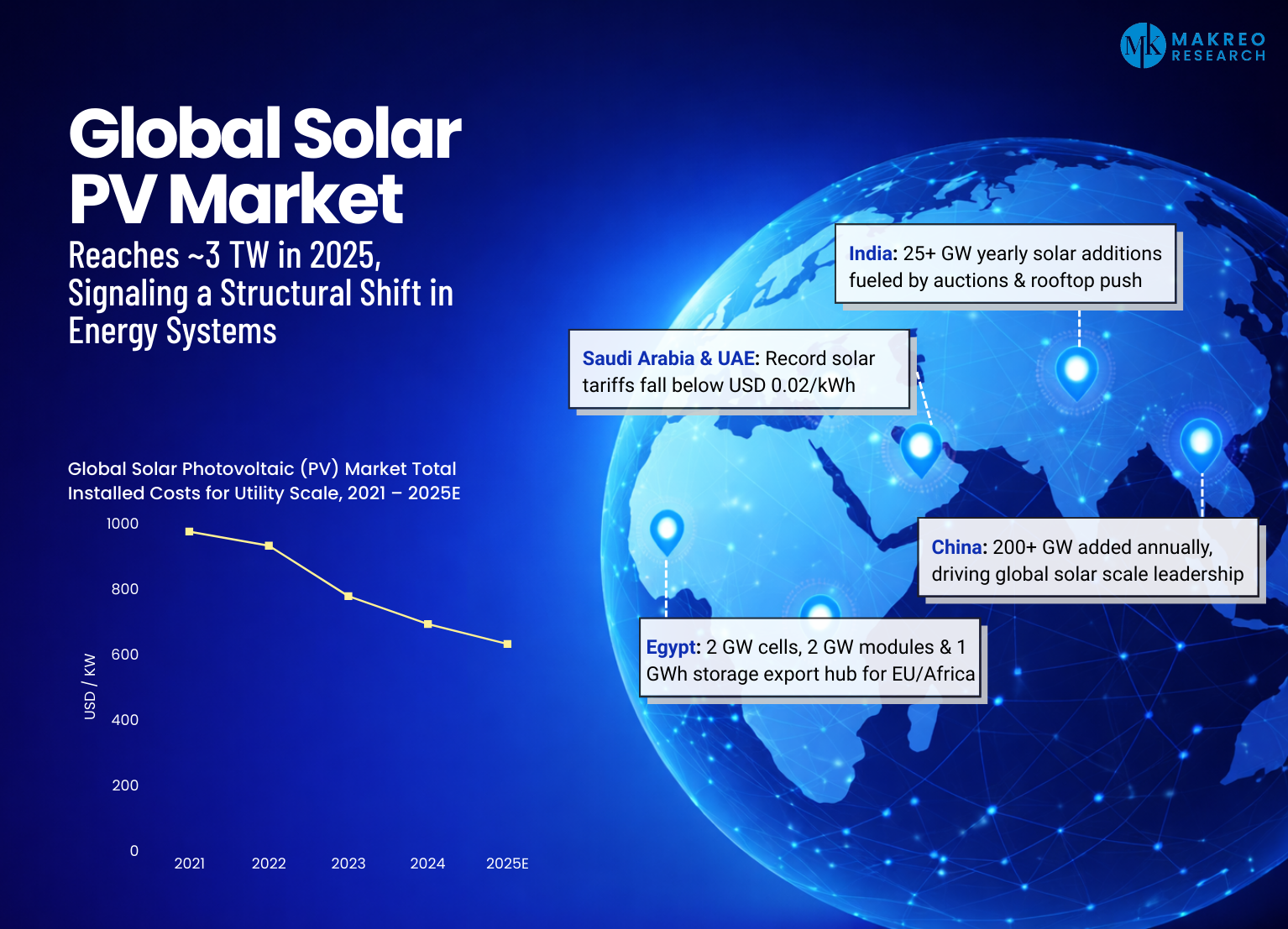

Asia Pacific remains the primary engine of global solar PV market growth. Between 2020 and 2024, the region consistently accounted for the largest share of annual solar capacity additions worldwide. According to Makreo Research, Asia Pacific added approximately 430 GW of new solar PV capacity in 2024 alone, reinforcing its dominance in global deployment volumes.

China continued to lead in absolute installations, while India and Southeast Asia emerged as increasingly important sources of incremental demand. However, 2025 marks a subtle but meaningful transition. While aggregate demand remains strong, growth trajectories across the region are becoming less uniform.

China’s additions remain substantial, but pricing pressure and manufacturing oversupply are compressing margins. India, in contrast, is entering a phase of structurally accelerated growth, driven by policy-backed manufacturing expansion alongside rising domestic demand. Southeast Asian markets are scaling more selectively, influenced by grid readiness and financing constraints.

Asia Pacific still anchors global solar volumes, but the drivers of growth are diverging sharply by country.

China Solar PV Market: Manufacturing Scale Persists as Margins Tighten

China continues to dominate the global solar PV supply chain, controlling over 80% of polysilicon, wafer, cell, and module manufacturing capacity. This scale has pushed global module prices to historic lows, reaching approximately USD 0.09/Wdc in late 2024, cementing solar PV as the most cost-competitive source of new power generation in many markets.

Yet 2025 exposed a structural contradiction. Despite record shipment volumes, China’s top four solar manufacturers collectively reported losses exceeding USD 1.5 billion in the first half of 2025. Intense price competition, excess capacity, and declining margins are redefining the economics of scale.

At the same time, geopolitical and regulatory scrutiny intensified. US forced-labor compliance measures, European ESG due-diligence frameworks, and cybersecurity concerns surrounding inverter hardware are increasing operational and compliance risks for Chinese exporters.

As a result, scale alone is no longer sufficient. Profitability, regulatory alignment, and geographic diversification are becoming equally critical.

Global Solar PV Manufacturing Diversifies Amid Trade Barriers and ESG Pressures

One of the clearest signals of structural change in 2025 has been the renewed globalization of solar manufacturing, driven not by cost optimization, but by defensive strategy.

Chinese manufacturers are increasingly establishing production bases outside traditional Asian hubs to mitigate trade barriers and regulatory exposure. A prominent example is JA Solar’s joint venture in Egypt, which includes 2 GW of solar cell capacity, 2 GW of module production, and 1 GWh of energy storage manufacturing, primarily oriented toward export markets.

Egypt’s strategic advantages, exemption from US AD/CVD duties, proximity to Europe and Africa, and growing policy support, make it an attractive manufacturing alternative. Similar investment patterns are emerging across the Middle East, India, and parts of Southeast Asia.

Manufacturing geography is becoming as important as manufacturing scale, signaling a structural rebalancing of the global solar PV supply chain.

India Solar PV Market Shifts from Demand Growth to Integrated Manufacturing

India’s solar PV market stands out in 2025 for the depth and balance of its growth. The country added approximately 35 GW of solar capacity in the first 11 months of 2025, representing a 67% year-on-year increase and taking cumulative installations to nearly 133 GW.

Solar PV now accounts for more than half of India’s total renewable energy capacity, pushing the country past the 100 GW milestone ahead of schedule. What distinguishes India’s trajectory is the simultaneous scaling of domestic manufacturing.

Module nameplate capacity reached 144 GW, solar cell manufacturing crossed 24 GW, and over 81 GW of new module capacity was added in 2025 alone. Policy support through the Production Linked Incentive (PLI) scheme has accelerated localization, although gaps remain in polysilicon and wafer production.

India is no longer just a high-growth demand market. It is positioning itself as a strategic manufacturing counterweight within the global solar ecosystem.

Europe’s Solar PV Market Becomes System-Critical as Storage and Grid Stability Rise

In Europe, solar PV growth in 2025 was defined less by headline installation numbers and more by system-level impact. Germany installed approximately 16.2 GW of new solar capacity, sustaining momentum from 2024. More significantly, solar PV generated 87 TWh of electricity, surpassing coal generation across the European Union for the first time.

On peak days, solar met over 98% of instantaneous grid demand in Germany, an outcome that would have been inconceivable just five years earlier. This level of penetration is forcing a fundamental rethink of grid operations.

Self-consumption rates are rising, residential and commercial battery installations grew by over 60% year-on-year, and nearly 25 GWh of battery storage is now installed across the region. Solar PV is no longer viewed solely as a decarbonization tool; it has become a core pillar of grid stability, price moderation, and energy security.

US Solar PV Market Faces Policy Uncertainty as IRA Rules Tighten

While global solar economics continue to strengthen, policy risk re-emerged sharply in the United States in 2025. Following the passage of the “One Big Beautiful Bill Act,” executive actions tightened eligibility criteria for Inflation Reduction Act (IRA) tax credits.

Stricter interpretations of “beginning of construction” requirements and Foreign Entity of Concern (FEOC) rules have introduced uncertainty across utility-scale project pipelines. Industry analysts estimate that up to 60 GW of planned solar capacity could face delays or cancellation by 2030 if restrictive interpretations persist.

Despite this uncertainty, underlying fundamentals remain strong. Utility-scale solar levelized cost of electricity (LCOE) tightened further in 2025, ranging between USD 38 and 78 per MWh, keeping solar among the most competitive generation technologies in the US.

The near-term outcome is a surge in project execution ahead of policy deadlines, creating a volatile but active deployment environment through 2026.

Solar-Plus-Storage Becomes the Default Utility-Scale PV Model

One of the most consequential structural shifts underway is the rapid mainstreaming of solar paired with battery energy storage systems (BESS). Battery pack prices have declined by approximately 93% since 2010, reaching around USD 192 per kWh for utility-scale systems in 2024.

Combined with record-low module prices, solar-plus-storage projects are now competitive not only on energy costs, but also on capacity, flexibility, and reliability. This transformation is particularly significant in emerging markets with weak grids, data centers seeking round-the-clock clean power, and regions phasing out diesel peaking plants.

Large-scale hybrid projects across Africa, including Rwanda and Egypt, demonstrate that storage-backed solar is now bankable infrastructure rather than an experimental add-on.

Solar PV Technology Trends Reshape Costs and Supply Dependencies

While deployment headlines dominate public discourse, technology evolution continues to reshape solar economics behind the scenes. TOPCon and bifacial modules are improving yields, but 2025 also highlighted reliability challenges, including UV-induced degradation, prompting greater investment in materials science and long-term performance testing.

Innovation is also moving upstream. Efforts to replace silver with copper in cell metallization could significantly alter solar supply chains. If commercialized at scale, copper-based designs would reduce material costs, lower import dependence, and reshape manufacturing economics, particularly in China and India.

These incremental technology shifts are reinforcing solar’s competitiveness while subtly redefining supply-chain dependencies.

Solar PV’s Next Decade Will Be Defined by Execution, Not Adoption

Despite short-term volatility around policy, pricing, and supply chains, the global solar PV market remains structurally aligned for sustained expansion through 2030, as assessed by Makreo Research. Asia Pacific will continue to function as the global scale engine, while markets such as India, Europe, and select MENA regions emerge as execution-led growth centers.

In these markets, grid integration, storage adoption, and manufacturing localization are becoming more important than raw installation volumes. Solar PV is transitioning from a marginal generation source into foundational energy infrastructure, supporting grid stability, decarbonization pathways, and long-term energy security.

Makreo Research’s study, “Global Solar Photovoltaic (PV) Market Size and Forecast (2021–2030)”, delivers a comprehensive assessment of deployment models, technology pathways, regional dynamics, investments, and competitive positioning shaping this transition.

The analysis highlights a clear shift from volume-driven growth toward execution-led market leadership. The decisive question ahead is no longer whether solar will continue to scale, but which markets and players can scale it efficiently, reliably, and sustainably in an increasingly complex global energy landscape.

Market Segmentation of Global Solar PV Market

By Application

-

Utility-Scale

-

Residential, Commercial & Industrial

By Deployment Model

-

Ground Mounted

-

Rooftop

By Regions

-

Asia Pacific

-

Europe

-

North America

-

Other Regions

Competitive Landscape

-

Competition Section

-

Mergers, Acquisitions, and Investments

-

Funding Timeline

-

Company Profiles

Companies Covered:

-

Jinko Solar Holding Co., Ltd.

-

JA Solar Technology Co., Ltd.

-

Canadian Solar Inc.

-

LONGi Green Energy Technology Co., Ltd

-

Trina Solar Co., Ltd.

The study covers a total of 12 Global Solar PV Market companies.

Global Solar PV Market, Solar PV Market Size, Solar Photovoltaic Market, Global Solar Energy Market, Solar Power Market 2025, Solar PV Market Forecast 2030, Global Solar PV Capacity, Utility-Scale Solar Market, Asia Pacific Solar PV Market, China Solar PV Market, India Solar PV Market, Europe Solar PV Market, US Solar PV Market, Middle East Solar PV Market, Egypt Solar Manufacturing Hub, Global Solar Manufacturing Capacity, Solar PV Supply Chain Diversification, Solar Module Manufacturing Trends, Solar Cell Manufacturing Market, Solar Manufacturing Localization, Solar Trade Barriers, ESG Compliance Solar Industry, Solar Plus Storage Market, Battery Energy Storage Systems BESS, Utility-Scale Solar Storage, Hybrid Solar Power Plants, Solar PV Technology Trends, TOPCon Solar Modules, Bifacial Solar Panels Market, Solar Module Prices, Solar LCOE Trends, Renewable Energy Market Trends, Clean Energy Transition, Global Solar Investment Trends, Grid Integration of Solar Power, Energy Infrastructure Transition