Global Mattress Market Nears USD 78 Billion as Premiumisation and Omnichannel Control Redefine Demand

Explore how the global mattress market is shifting toward sleep health, sustainability, material innovation, and larger sizes, redefining value, comfort, and buying behavior.

For decades, the mattress market operated quietly in the background of consumer industries, rarely discussed, infrequently purchased, and largely viewed as a functional household item rather than a strategic product category. That perception is now decisively shifting. Across global markets, mattresses are being repositioned as sleep-health solutions, sustainability pressure points, and distribution-sensitive assets, placing the category at the convergence of wellness, material science, and retail transformation. With global mattress ownership already covering ~71.3% of households, future growth is no longer driven by penetration, but by how, why, and where consumers upgrade, creating a more competitive and structurally complex market than ever before.

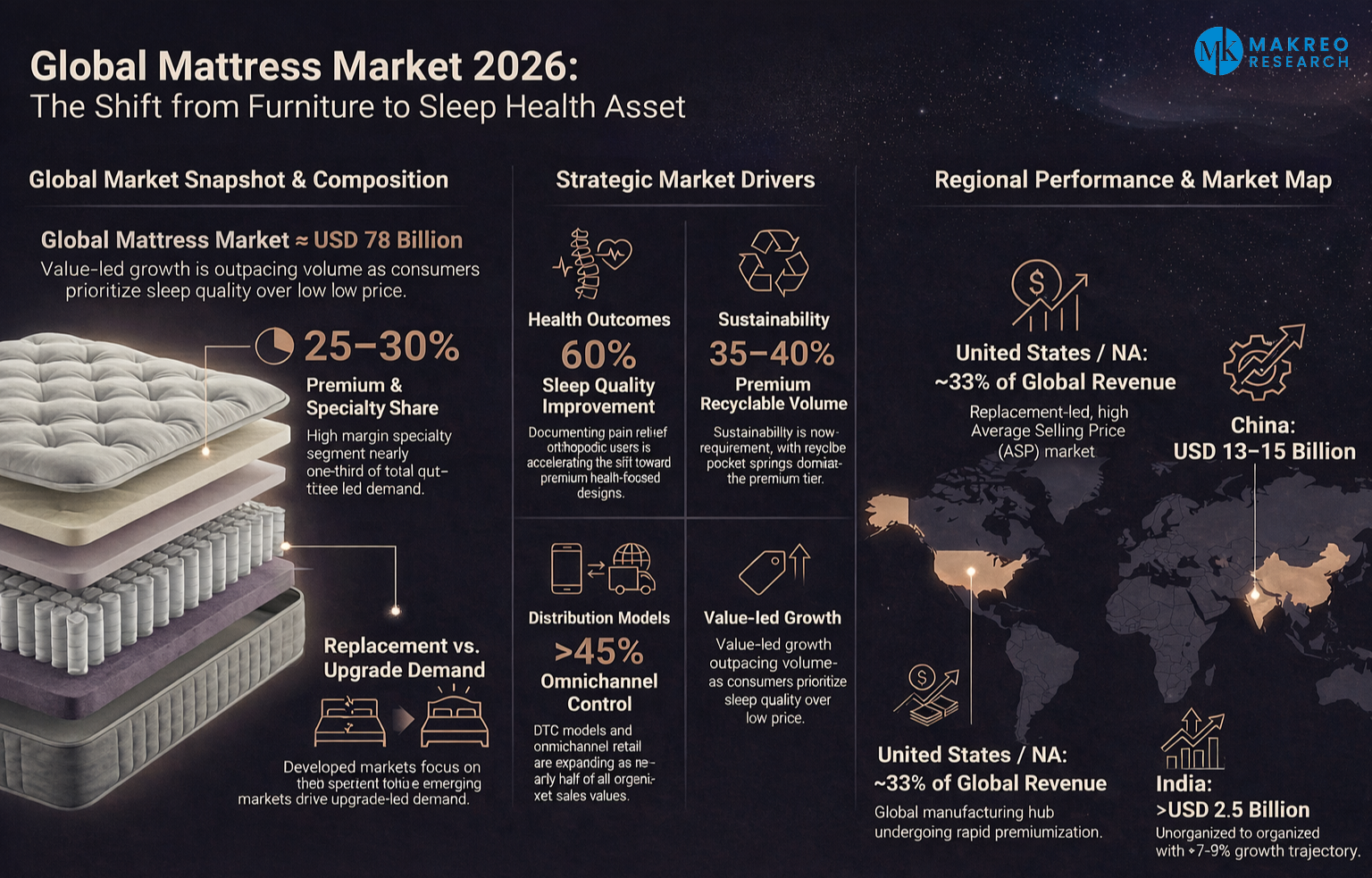

Makreo Research’s synthesis of global mattress industry signals shows demand moving away from price and age driven replacement cycles toward comfort, health, and lifestyle led decision-making. While developed markets remain replacement-heavy with household penetration exceeding 85%, emerging economies are adding incremental demand through urban housing expansion and organised retail growth. Premium and specialty mattresses now account for ~25-30% of global revenues, confirming a structural pivot from volume-led growth to value-led monetisation.

Key Structural Trends Reshaping the Global Mattress Market

1. Sleep Health Is Superseding Price as the Core Purchase Driver

Mattresses are increasingly assessed through sleep quality, pain relief, posture support, and physical recovery. Clinical research indicates that mattress upgrades can improve sleep quality by ~60% among chronic pain users, accelerating demand for orthopedic, hybrid, and ergonomic mattress designs. As a result, premium and specialty products contribute ~25-30% of global mattress revenues, even as affordability remains critical in mass-market segments.

2. Sustainability and Waste Reduction Are Becoming Structural Requirements

Globally, mattresses rank among the most difficult household products to recycle, intensifying regulatory scrutiny and accelerating material innovation. Pocket-spring mattresses already represent ~35-40% of global premium volumes, with recyclability and mono-material construction emerging as decisive differentiators. Circular-economy initiatives, including glue-free spring systems and recyclable foams, are increasingly shaping procurement and product development strategies, particularly across Europe and North America.

3. Distribution Power Is Shifting from Retail Dependence to Omnichannel Control

E-commerce and direct-to-consumer (DTC) models are reshaping pricing transparency, accessibility, and margin structures. In mature markets, vertically integrated manufacturers now control over 45% of organised mattress sales value, enabling tighter margin capture as average mid-tier mattress prices approach USD 1,000. Traditional retailer mark-ups alone range between USD 200-300 per unit, reinforcing the strategic importance of channel ownership.

4. Replacement Cycles Are Becoming Condition-Led Rather Than Time-Led

Conventional age-based replacement norms are weakening. Consumers increasingly replace mattresses based on comfort degradation, health triggers, and lifestyle upgrades rather than elapsed usage years. By 2025, physical wear and sleep discomfort emerged as the primary replacement drivers, while upgrade-driven purchases continue rising due to premiumisation and technology adoption.

Latex vs Hybrid vs PU Foam Mattress Comparison

Natural latex adoption is accelerating due to its durability, hygiene benefits, and sustainability credentials, while hybrid mattresses continue to dominate organised retail because of their balance between comfort and price. PU foam remains volume-led but is steadily losing share within higher-value and premium segments.

The Super-Sized Mattress Shift - Why 2026 Is Redefining Sleep Space Economics?

The rise of super-sized mattresses in 2026 is not a design indulgence, it reflects a data-backed correction to decades of undersized sleep surfaces. Consumer trends highlighted by John Lewis show double-mattress sales declining by 5%, while king-size demand has increased by 23% and super-king sales have surged by 39% year-on-year. Buyers are no longer upgrading incrementally; they are moving directly to maximum space.

The underlying driver is sleep geometry. On a standard double mattress, two adults share roughly 67.5 cm of width each. A super-king expands this to 90 cm per person, a 33% increase in individual sleep space without extending sleep duration. That additional width directly reduces involuntary contact, roll disturbance, and micro-awakenings, critical inhibitors of deep sleep quality.

What most consumers overlook:

- A 33% increase in lateral space can reduce partner-movement disruption by double-digit percentages, according to sleep-comfort testing benchmarks

- Wider mattresses consistently outperform upgrades in foam density or firmness alone in long-term comfort reviews

- Super-king mattresses effectively provide single-bed width per sleeper while retaining a shared sleep surface

Notably, adoption is being driven by urban couples and even solo sleepers, indicating a clear trade-off: floor space is being exchanged for sleep continuity, recovery, and long-term comfort.

By 2026, the mattress is no longer passive furniture, it is evolving into a precision sleep asset. The data suggests this is not a temporary preference, but a structural reset in how consumers quantify rest, comfort, and personal space.

United States Mattress Market

Why North America Continues to Anchor Global Value?

North America contributes roughly one-third of global mattress revenues, with the United States accounting for over 80% of regional value. Demand remains predominantly replacement-led, supported by institutional buyers, rental housing, and hospitality sectors. While shipment growth is expected to remain flat through 2026, stable volumes and high average selling prices (ASPs) continue to define regional performance. North America’s premium positioning, strong retail distribution networks, and high per-capita mattress spending sustain its outsized share of global industry value, even as mature demand limits volume expansion.

China Mattress Market

How the Scale Converges with Manufacturing Strength?

China’s mattress market is valued at approximately USD 13.6-15.2 billion in 2024, and is projected to expand to ~USD 18-20 billion by 2026-2030, with compound annual growth rates in the ~6.5-8.2 % range driven by rising urban incomes, wellness-oriented consumer preferences, and strong e-commerce adoption. As the second-largest global consumption market, China also plays a significant role as a manufacturing hub, mattress production and component industries have shown steady value growth, supported by both domestic construction demand and export activity.

India Mattress Market

How is Growth Driven by Structural Market Transition?

India’s mattress market exceeds USD 2.5 billion in 2024-26 and is expected to grow robustly toward ~USD 3.5-5.8 billion by the early 2030, with compound annual growth rates around 7.8 - 9 % driven by urbanisation, rising disposable incomes, and mounting awareness of sleep health. Although per-capita mattress spending remains relatively low (below USD 4), this indicates substantial long-term headroom for value growth. The market is still predominantly served by the unorganised sector, but organised retail and branded players are gaining share as consumers shift toward better-quality and warranty-backed products.

Strategic Moves by Key Players Reshaping Competitive Dynamics

-

Tempur Sealy International integrated AI-enabled sleep tracking across more than 300,000 smart beds through a USD 25 million technology investment.

-

South Bay International expanded its North American footprint via asset acquisitions, strengthening exposure to a market that sells ~30-35 million units annually.

-

Slumberzone committed ₹100 crore (~USD 12 million) toward domestic manufacturing expansion in India, targeting production capacity of ~1,000 units per day.

-

Spinks surpassed 100 patented innovations, introducing recyclable pocket-core systems aligned with both performance benchmarks and ESG mandates.

-

Somnigroup International reinforced its omnichannel dominance through a ~USD 5 billion acquisition of Mattress Firm, cementing vertical integration as a durable competitive moat.

What the Global Mattress Market Signals Going Forward?

The global mattress market has moved beyond cyclical, low-engagement dynamics. Consumers are upgrading for sleep quality, health outcomes, and spatial comfort, not merely replacing worn products, driving sustained increases in average selling prices.

Growth will remain uneven but structurally supported. Emerging markets will contribute incremental demand through urban housing and organised retail expansion, while developed economies monetise condition-led upgrades rather than time-based replacements. Mid-tier mattress prices in mature markets are approaching USD 1,000, while vertically integrated players now control over ~45% of organised sales value, reinforcing scale-driven margin advantages. Simultaneously, sustainability and durability are reshaping competition, with recyclable pocket-spring systems accounting for ~35-40% of premium volumes and longer-life materials encouraging fewer but higher-value purchases.

In effect, this market will grow selectively. Volume alone will no longer defend market share. Competitive advantage will increasingly depend on aligning product performance, pricing power, and distribution control with how consumers now assign value to sleep. The mattress industry is no longer passive, it is becoming a precision-driven sleep economy where value, not units, defines winners.

How Makreo Research Enables Confident Strategic Decisions

In a mattress market shaped by premiumisation, sustainability mandates, and distribution consolidation, Makreo Research delivers clarity beyond surface-level forecasting. Our Global Mattress Market Size and Forecast (2021-2030) provide granular insights into replacement behaviour, material cost economics, regional demand asymmetries, and competitive benchmarking, enabling firms to de-risk market entry, localise manufacturing, optimise pricing, and evaluate M&A opportunities with precision rather than assumption.

Our research supports:

-

Market entry and geographic expansion strategy

-

Manufacturing localisation and capex planning

-

Product portfolio structuring and pricing optimisation

-

Competitive benchmarking and M&A evaluation

As intuition loses relevance in an increasingly data-dense and margin-sensitive environment, Makreo helps industry leaders convert complexity into actionable strategy, supporting disciplined expansion, capital efficiency, and durable competitive positioning.

Email us at info@makreo.com to discuss your research needs and explore how we can become your research partner in progress.

Explore our Custom Research & Market Survey Capabilities

Global Mattress Market, Mattress Market Analysis, Mattress Market Forecast 2030, Mattress Industry Trends, Mattress Market Size and Outlook, Global Sleep Products Market, Mattress Industry Outlook, Latex Mattress Market, Hybrid Mattress Market, PU Foam Mattress Market, Pocket Spring Mattresses, Mattress Material Segmentation, Sleep Health Products, Mattress Replacement Cycles, Mattress Premiumisation, Sustainable Mattress Materials, Circular Economy in Mattresses, Recyclable Mattress Systems, Omnichannel Mattress Retail, DTC Mattress Market, Mattress Size Trends, Super King Mattress Market, Sleep Space Economics, United States Mattress Market, China Mattress Market, India Mattress Market, Mattress Industry Competitive Landscape, Mattress Industry Strategy, Mattress Industry M&A